Page 157 - DCOM302_MANAGEMENT_ACCOUNTING

P. 157

Management Accounting

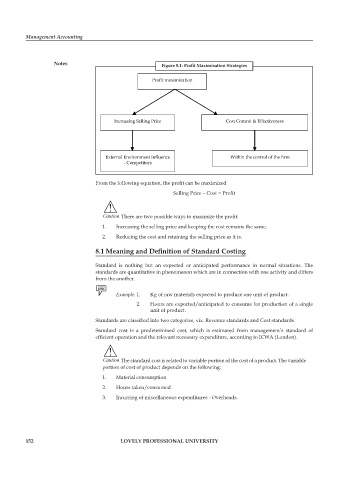

Notes Figure 8.1: Profit Maximisation Strategies

Profit maximization

Increasing Selling Price Cost Control & Effectiveness

External Environment Influence Within the control of the firm

- Competitors

From the following equation, the profit can be maximized

Selling Price – Cost = Profit

!

Caution There are two possible ways to maximize the profit:

1. Increasing the selling price and keeping the cost remains the same.

2. Reducing the cost and retaining the selling price as it is.

8.1 Meaning and Definition of Standard Costing

Standard is nothing but an expected or anticipated performance in normal situations. The

standards are quantitative in phenomenon which are in connection with one activity and differs

from the another.

Example: 1. Kg of raw materials expected to produce one unit of product.

2. Hours are expected/anticipated to consume for production of a single

unit of product.

Standards are classified into two categories, viz. Revenue standards and Cost standards.

Standard cost is a predetermined cost, which is estimated from management’s standard of

efficient operation and the relevant necessary expenditure, according to ICWA (London).

!

Caution The standard cost is related to variable portion of the cost of a product. The variable

portion of cost of product depends on the following:

1. Material consumption

2. Hours taken/consumed

3. Incurring of miscellaneous expenditures - Overheads.

152 LOVELY PROFESSIONAL UNIVERSITY