Page 120 - DCOM308_DCOM502_INDIRECT_TAX_LAWS

P. 120

85

86 Sale of space or time for advertisement 01.05.2006

Auctioneers’ Services

01.05.2006

87 ATM Operation, maintenance or management Services 01.05.2006

88 Business Support Services 01.05.2006

89 Credit Card, Debit Card, Charge Card or other payment 01.05.2006

Card Services Unit 7: Collection and Recovery of Service Tax and Assessment Procedure

90 Internet Telecommunication Services 01.05.2006

91 Public Relations Services 01.05.2006

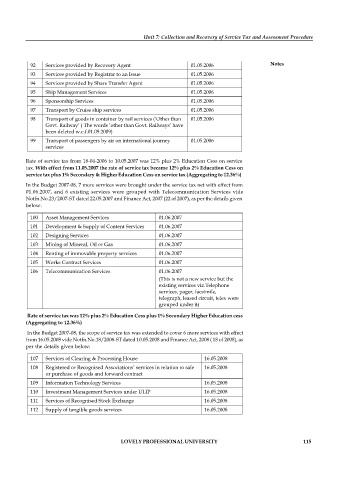

92 Services provided by Recovery Agent 01.05.2006 Notes

93 Services provided by Registrar to an Issue 01.05.2006

94 Services provided by Share Transfer Agent 01.05.2006

95 Ship Management Services 01.05.2006

96 Sponsorship Services 01.05.2006

97 Transport by Cruise ship services 01.05.2006

98 Transport of goods in container by rail services (‘Other than 01.05.2006

Govt. Railway’ ) The words ‘other than Govt. Railways’ have

been deleted w.e.f.01.09.2009)

99 Transport of passengers by air on international journey 01.05.2006

services

Rate of service tax from 18-04-2006 to 10.05.2007 was 12% plus 2% Education Cess on service

tax. With effect from 11.05.2007 the rate of service tax became 12% plus 2% Education Cess on

service tax plus 1% Secondary & Higher Education Cess on service tax (Aggregating to 12.36%)

In the Budget 2007-08, 7 more services were brought under the service tax net with effect from

01.06.2007, and 6 existing services were grouped with Telecommunication Services vide

Notfn.No.23/2007-ST dated 22.05.2007 and Finance Act, 2007 (22 of 2007), as per the details given

below:

100 Asset Management Services 01.06.2007

101 Development & Supply of Content Services 01.06.2007

102 Designing Services 01.06.2007

103 Mining of Mineral, Oil or Gas 01.06.2007

104 Renting of immovable property services 01.06.2007

105 Works Contract Services 01.06.2007

106 Telecommunication Services 01.06.2007

(This is not a new service but the

existing services viz.Telephone

services, pager, facsimile,

telegraph, leased circuit, telex were

grouped under it)

Rate of service tax was 12% plus 2% Education Cess plus 1% Secondary Higher Education cess

(Aggregating to 12.36%)

In the Budget 2007-08, the scope of service tax was extended to cover 6 more services with effect

from 16.05.2008 vide Notfn.No.18/2008-ST dated 10.05.2008 and Finance Act, 2008 ( 18 of 2008), as

per the details given below:

107 Services of Clearing & Processing House 16.05.2008

108 Registered or Recognised Associations’ services in relation to sale 16.05.2008

or purchase of goods and forward contract

109 Information Technology Services 16.05.2008

110 Investment Management Services under ULIP 16.05.2008

111 Services of Recognised Stock Exchange 16.05.2008

112 Supply of tangible goods services 16.05.2008

LOVELY PROFESSIONAL UNIVERSITY 115