Page 170 - DMGT207_MANAGEMENT_OF_FINANCES

P. 170

Unit 7: Concept of Leverages

8. The firms operating break-even point are the level of sale necessary to give all Notes

………………….. costs.

7.3 Financial Leverage

Financial leverage is defined as the ability of a firm to use fixed financial charges to magnify the

effects in EBIT/operating profits, on the firm’s earning per share, the two fixed financial cost that

may be found in the firms income statement are:

1. Interest on debt and

2. Dividends on preferred shares.

These charges must be paid regardless of the amount of EBIT available to pay them.

Notes The financial leverage is favourable when the firm earns more on the investments/

assets financed by the sources having fixed charges. It is obvious that shareholders gain in

a situation where a company earns a higher rate of return and pays a low rate to the

supplier of long term funds. Financial leverage in such cases is also called “trading in

equity.”

The degree of financial leverage is the nursical measure of the firms’ financial leverage and is

calculated as:

Financial leverage =

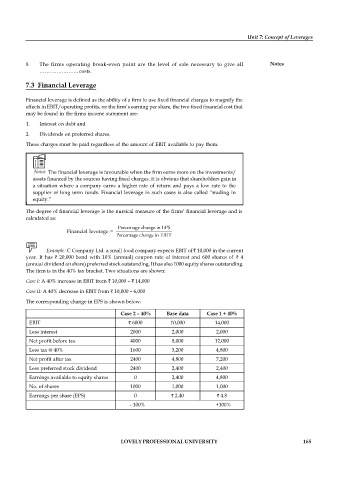

Example: C Company Ltd. a small food company expects EBIT of 10,000 in the current

year. It has 20,000 bond with 10% (annual) coupon rate of interest and 600 shares of 4

(annual dividend on share) preferred stock outstanding. It has also 1000 equity shares outstanding.

The firm is in the 40% tax bracket. Two situations are shown:

Case I: A 40% increase in EBIT from 10,000 – 14,000

Case II: A 40% decrease in EBIT from 10,000 – 6,000

The corresponding change in EPS is shown below:

Case 2 – 40% Base data Case 1 + 40%

EBIT 6000 10,000 14,000

Less interest 2000 2,000 2,000

Net profit before tax 4000 8,000 12,000

Less tax @ 40% 1600 3,200 4,800

Net profit after tax 2400 4,800 7,200

Less preferred stock dividend 2400 2,400 2,400

Earnings available to equity shares 0 2,400 4,800

No. of shares 1000 1,000 1,000

Earnings per share (EPS) 0 2.40 4.8

– 100% +100%

LOVELY PROFESSIONAL UNIVERSITY 165