Page 343 - DCOM201_ACCOUNTING_FOR_COMPANIES_I

P. 343

Particulars

Previous Year

Current Year

No.

2

4

3

1. Share Holders Funds

Share Capital + Reserves and Surplus

2. Loan Funds

I. Sources of Funds 1 Schedule Figures for the Figures for the

(a) Secured Loans

(b) Unsecured Loans

Total

II. Application of Funds:

1. Fixed Assets

Accounting for Companies-I

(a) Gross Block

(b) Less Depreciation

(c) Net Block

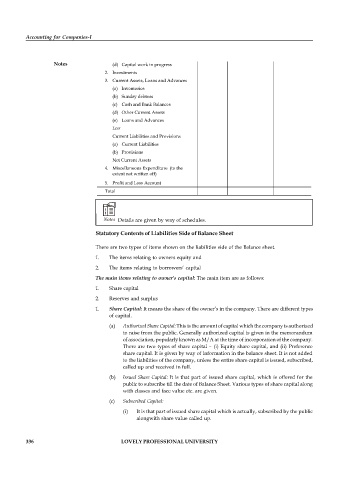

Notes (d) Capital work in progress

2. Investments

3. Current Assets, Loans and Advances

(a) Inventories

(b) Sundry debtors

(c) Cash and Bank Balances

(d) Other Current Assets

(e) Loans and Advances

Less

Current Liabilities and Provisions

(a) Current Liabilities

(b) Provisions

Net Current Assets

4. Miscellaneous Expenditure (to the

extent not written off)

5. Profit and Loss Account

Total

Notes Details are given by way of schedules.

Statutory Contents of Liabilities Side of Balance Sheet

There are two types of items shown on the liabilities side of the Balance sheet.

1. The items relating to owners equity and

2. The items relating to borrowers’ capital

The main items relating to owner’s capital: The main item are as follows:

1. Share capital

2. Reserves and surplus

1. Share Capital: It means the share of the owner’s in the company. There are different types

of capital.

(a) Authorized Share Capital: This is the amount of capital which the company is authorized

to raise from the public. Generally authorized capital is given in the memorandum

of association, popularly known as M/A at the time of incorporation of the company.

There are two types of share capital – (i) Equity share capital, and (ii) Preference

share capital. It is given by way of information in the balance sheet. It is not added

to the liabilities of the company, unless the entire share capital is issued, subscribed,

called up and received in full.

(b) Issued Share Capital: It is that part of issued share capital, which is offered for the

public to subscribe till the date of Balance Sheet. Various types of share capital along

with classes and face value etc. are given.

(c) Subscribed Capital:

(i) It is that part of issued share capital which is actually, subscribed by the public

alongwith share value called up.

336 LOVELY PROFESSIONAL UNIVERSITY