Page 158 - DCOM207_LABOUR_LAWS

P. 158

Unit 9: Payment of Bonus Act, 1965

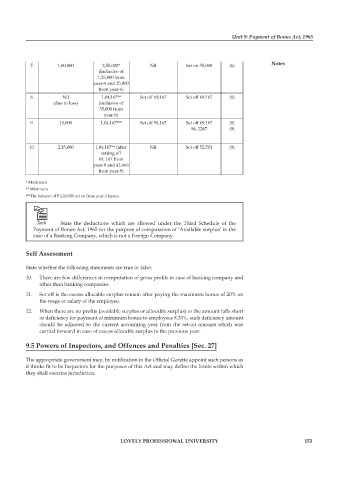

7. 1,00,000 2,50,000* Nil Set on 35,000 (6) Notes

(Inclusive of

1,25,000 from

year-4 and 25,000

from year-6)

8. Nil 1,04,167** Set off 69,167 Set off 69,167 (8)

(due to loss) (inclusive of

35,000 from

year-6)

9. 10,000 1,04,167*** Set off 94,167 Set off 69,167 (8)

94, 1267 (9)

10. 2,15,000 1,04,167** (after Nil Set off 52,501 (9)

setting off

69, 167 from

year-8 and 41,666

from year-9)

* Maximum

** Minimum

***The balance of ` 1,10,000 set on from year-2 lapses.

Task State the deductions which are allowed under the Third Schedule of the

Payment of Bonus Act, 1965 for the purpose of computation of ‘Available surplus’ in the

case of a Banking Company, which is not a Foreign Company.

Self Assessment

State whether the following statements are true or false:

10. There are few differences in computation of gross profits in case of banking company and

other than banking companies.

11. Set off is the excess allocable surplus remain after paying the maximum bonus of 20% on

the wage or salary of the employee.

12. When there are no profits (available surplus or allocable surplus) or the amount falls short

or deficiency for payment of minimum bonus to employees 8.33%, such deficiency amount

should be adjusted to the current accounting year from the set-on amount which was

carried forward in case of excess allocable surplus in the previous year.

9.5 Powers of Inspectors, and Offences and Penalties [Sec. 27]

The appropriate government may, by notification in the Official Gazette appoint such persons as

it thinks fit to be Inspectors for the purposes of this Act and may define the limits within which

they shall exercise jurisdiction.

LOVELY PROFESSIONAL UNIVERSITY 153