Page 156 - DCOM509_ADVANCED_AUDITING

P. 156

Unit 9: Audit of Limited Companies

Notes

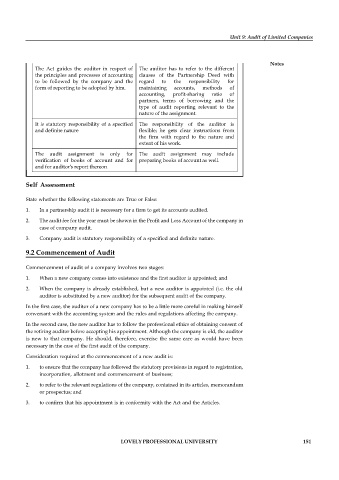

The Act guides the auditor in respect of The auditor has to refer to the different

the principles and processes of accounting clauses of the Partnership Deed with

to be followed by the company and the regard to the responsibility for

form of reporting to be adopted by him. maintaining accounts, methods of

accounting, profit-sharing ratio of

partners, terms of borrowing and the

type of audit reporting relevant to the

nature of the assignment.

It is statutory responsibility of a specified The responsibility of the auditor is

and definite nature flexible; he gets clear instructions from

the firm with regard to the nature and

extent of his work.

The audit assignment is only for The audit assignment may include

verification of books of account and for preparing books of account as well.

and for auditor's report thereon

Self Assessment

State whether the following statements are True or False:

1. In a partnership audit it is necessary for a firm to get its accounts audited.

2. The audit fee for the year must be shown in the Profit and Loss Account of the company in

case of company audit.

3. Company audit is statutory responsibility of a specified and definite nature.

9.2 Commencement of Audit

Commencement of audit of a company involves two stages:

1. When a new company comes into existence and the first auditor is appointed; and

2. When the company is already established, but a new auditor is appointed (i.e. the old

auditor is substituted by a new auditor) for the subsequent audit of the company.

In the first case, the auditor of a new company has to be a little more careful in making himself

conversant with the accounting system and the rules and regulations affecting the company.

In the second case, the new auditor has to follow the professional ethics of obtaining consent of

the retiring auditor before accepting his appointment. Although the company is old, the auditor

is new to that company. He should, therefore, exercise the same care as would have been

necessary in the case of the first audit of the company.

Consideration required at the commencement of a new audit is:

1. to ensure that the company has followed the statutory provisions in regard to registration,

incorporation, allotment and commencement of business;

2. to refer to the relevant regulations of the company, contained in its articles, memorandum

or prospectus; and

3. to confirm that his appointment is in conformity with the Act and the Articles.

LOVELY PROFESSIONAL UNIVERSITY 151