Page 231 - DMGT104_FINANCIAL_ACCOUNTING

P. 231

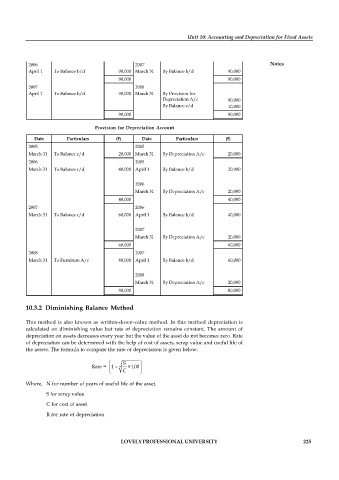

Date Particulars ( ) Date Particulars ( )

2004 2005

April 1 To Bank A/c 90,000 March 31 By Balance c/d 90,000

90,000 90,000

Unit 10: Accounting and Depreciation for Fixed Assets

2005 2006

April 1 To Balance b/d 90,000 March 31 By Balance c/d 90,000

90,000 90,000

2006 2007 Notes

April 1 To Balance b/d 90,000 March 31 By Balance b/d 90,000

90,000 90,000

2007 2008

April 1 To Balance b/d 90,000 March 31 By Provision for

Depreciation A/c 80,000

By Balance c/d 10,000

90,000 90,000

Provision for Depreciation Account

Date Particulars ( ) Date Particulars ( )

2005 2005

March 31 To Balance c/d 20,000 March 31 By Depreciation A/c 20,000

2006 2005

March 31 To Balance c/d 40,000 April 1 By Balance b/d 20,000

2006

March 31 By Depreciation A/c 20,000

40,000 40,000

2007 2006

March 31 To Balance c/d 60,000 April 1 By Balance b/d 40,000

2007

March 31 By Depreciation A/c 20,000

60,000 60,000

2008 2007

March 31 To Furniture A/c 80,000 April 1 By Balance b/d 60,000

2008

March 31 By Depreciation A/c 20,000

80,000 80,000

10.3.2 Diminishing Balance Method

This method is also known as written-down-value method. In this method depreciation is

calculated on diminishing value but rate of depreciation remains constant. The amount of

depreciation on assets decreases every year but the value of the asset do not becomes zero. Rate

of depreciation can be determined with the help of cost of assets, scrap value and useful life of

the assets. The formula to compute the rate of depreciation is given below:

æ S ö

Rate = 1 – n C × 100 ÷ ø

ç

è

Where, N for number of years of useful life of the asset.

S for scrap value

C for cost of asset

R for rate of depreciation

LOVELY PROFESSIONAL UNIVERSITY 225