Page 169 - DMGT202_COST_AND_MANAGEMENT_ACCOUNTING

P. 169

Cost and Management Accounting

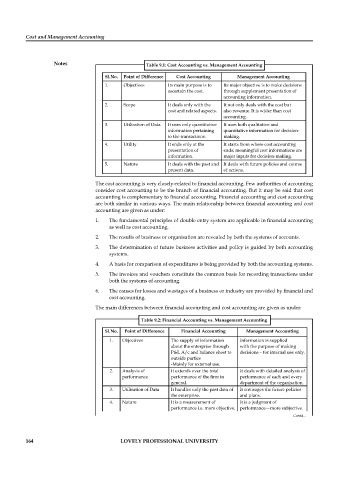

Notes Table 9.1: Cost Accounting vs. Management Accounting

Sl.No. Point of Difference Cost Accounting Management Accounting

1. Objectives Its main purpose is to Its major objective is to make decisions

ascertain the cost. through supplement presentation of

accounting information.

2. Scope It deals only with the It not only deals with the cost but

cost and related aspects. also revenue. It is wider than cost

accounting.

3. Utilisation of Data It uses only quantitative It uses both qualitative and

information pertaining quantitative information for decision-

to the transactions. making.

4. Utility It ends only at the It starts from where cost accounting

presentation of ends; meaningful cost informations are

information. major inputs for decision-making.

5. Nature It deals with the past and It deals with future policies and course

present data. of actions.

The cost accounting is very closely-related to financial accounting. Few authorities of accounting

consider cost accounting to be the branch of financial accounting. But it may be said that cost

accounting is complementary to financial accounting. Financial accounting and cost accounting

are both similar in various ways. The main relationship between financial accounting and cost

accounting are given as under:

1. The fundamental principles of double entry system are applicable in fi nancial accounting

as well as cost accounting.

2. The results of business or organisation are revealed by both the systems of accounts.

3. The determination of future business activities and policy is guided by both accounting

systems.

4. A basis for comparison of expenditures is being provided by both the accounting systems.

5. The invoices and vouchers constitute the common basis for recording transactions under

both the systems of accounting.

6. The causes for losses and wastages of a business or industry are provided by fi nancial and

cost accounting.

The main differences between financial accounting and cost accounting are given as under:

Table 9.2: Financial Accounting vs. Management Accounting

Sl.No. Point of Difference Financial Accounting Management Accounting

1. Objectives The supply of information Information is supplied

about the enterprise through with the purpose of making

P&L A/c and balance sheet to decisions – for internal use only.

outside parties

-Mainly for external use.

2. Analysis of It extends over the total It deals with detailed analysis of

performance performance of the fi rm in performance of each and every

general. department of the organisation.

3. Utilisation of Data It handles only the past data of It envisages the future policies

the enterprise. and plans.

4. Nature It is a measurement of It is a judgment of

performance i.e. more objective. performance—more subjective.

Contd...

164 LOVELY PROFESSIONAL UNIVERSITY