Page 170 - DMGT202_COST_AND_MANAGEMENT_ACCOUNTING

P. 170

Unit 9: Introduction to Management Accounting

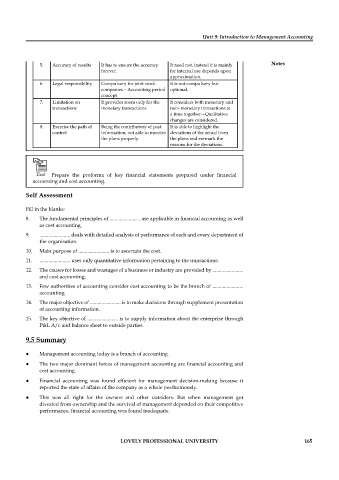

5. Accuracy of results It has to ensure the accuracy It need not, instead it is mainly Notes

forever. for internal use depends upon

approximation.

6. Legal responsibility Compulsory for joint stock It is not compulsory but

companies – Accounting period optional.

concept.

7. Limitation on It provides room only for the It considers both monetary and

transactions monetary transactions. non- monetary transactions at

a time together—Qualitative

changes are considered.

8. Exercise the path of Being the contributory of past It is able to highlight the

control information; not able to monitor deviations of the actual from

the plans properly. the plans and earmark the

reasons for the deviations.

Task Prepare the proforma of key fi nancial statements prepared under fi nancial

accounting and cost accounting.

Self Assessment

Fill in the blanks:

8. The fundamental principles of ........................ are applicable in financial accounting as well

as cost accounting.

9. ........................ deals with detailed analysis of performance of each and every department of

the organisation.

10. Main purpose of ........................ is to ascertain the cost.

11. ........................ uses only quantitative information pertaining to the transactions.

12. The causes for losses and wastages of a business or industry are provided by ........................

and cost accounting.

13. Few authorities of accounting consider cost accounting to be the branch of ........................

accounting.

14. The major objective of ........................ is to make decisions through supplement presentation

of accounting information.

15. The key objective of ........................ is to supply information about the enterprise through

P&L A/c and balance sheet to outside parties.

9.5 Summary

Management accounting today is a branch of accounting.

The two major dominant forces of management accounting are financial accounting and

cost accounting.

Financial accounting was found efficient for management decision-making because it

reported the state of affairs of the company as a whole posthumously.

This was all right for the owners and other outsiders. But when management got

divested from ownership and the survival of management depended on their competitive

performance, financial accounting was found inadequate.

LOVELY PROFESSIONAL UNIVERSITY 165