Page 191 - DMGT202_COST_AND_MANAGEMENT_ACCOUNTING

P. 191

Cost and Management Accounting

Notes

Introduction

The ratio analysis is one of the important tools of financial statement analysis to study the fi nancial

stature of the business fleeces, corporate houses and so on.

According to J. Batty, “The term accounting ratio is used to describe signifi cant relationships

which exist between figures shown in a balance sheet, in a profit and loss account, in a budgetary

control system or in any other part of the accounting organization”.

Financial statements contain substantial information (figures) relating to profit or loss and fi nancial

position of the business. If these items in financial statements are considered independently it

may or may not be of much use. To make a meaningful reading of financial statements, these

items found in financial statements have to be compared with one another. Ratio analysis, as

a technique or analysis of fi nancial statement uses this method of comparing the various items

found in fi nancial statements.

11.1 Defi nition

According to J. Betty, “The term accounting is used to describe relationships signifi cantly which

exist in between figures shown in a balance sheet, Profit & Loss A/c, Trading A/c, Budgetary

control system or in any part of the accounting organization.”

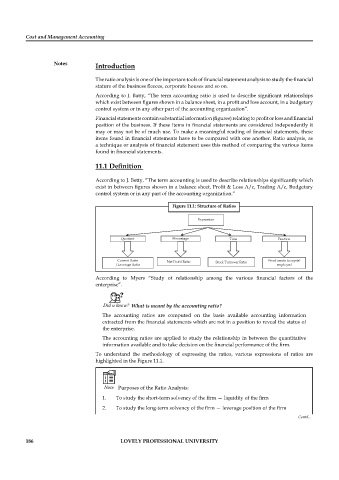

Figure 11.1: Structure of Ratios

According to Myers “Study of relationship among the various financial factors of the

enterprise”.

Did u know? What is meant by the accounting ratio?

The accounting ratios are computed on the basis available accounting information

extracted from the fi nancial statements which are not in a position to reveal the status of

the enterprise.

The accounting ratios are applied to study the relationship in between the quantitative

information available and to take decision on the financial performance of the fi rm.

To understand the methodology of expressing the ratios, various expressions of ratios are

highlighted in the Figure 11.1.

Note Purposes of the Ratio Analysis:

1. To study the short-term solvency of the firm — liquidity of the fi rm

2. To study the long-term solvency of the firm — leverage position of the fi rm

Contd...

186 LOVELY PROFESSIONAL UNIVERSITY