Page 154 - DMGT549_INTERNATIONAL_FINANCIAL_MANAGEMENT

P. 154

Unit 9: Interest Rate and Currency Swaps

Notes

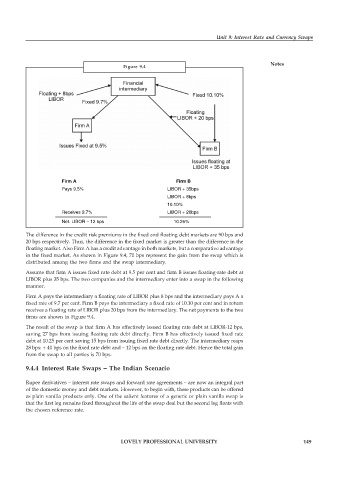

Figure 9.4

Firm A Firm B

Pays 9.5% LIBOR + 35bps

LIBOR + 8bps

10.10%

Receives 9.7% LIBOR + 20bps

Net. LIBOR – 12 bps 10.25%

The difference in the credit risk premiums in the fixed and floating debt markets are 90 bps and

20 bps respectively. Thus, the difference in the fixed market is greater than the difference in the

floating market. Also Firm A has a credit advantage in both markets, but a comparative advantage

in the fixed market. As shown in Figure 9.4, 70 bps represent the gain from the swap which is

distributed among the two firms and the swap intermediary.

Assume that firm A issues fixed rate debt at 9.5 per cent and firm B issues floating-rate debt at

LIBOR plus 35 bps. The two companies and the intermediary enter into a swap in the following

manner.

Firm A pays the intermediary a floating rate of LIBOR plus 8 bps and the intermediary pays A a

fixed rate of 9.7 per cent. Firm B pays the intermediary a fixed rate of 10.10 per cent and in return

receives a floating rate of LIBOR plus 20 bps from the intermediary. The net payments to the two

firms are shown in Figure 9.4.

The result of the swap is that firm A has effectively issued floating rate debt at LIBOR-12 bps,

saving 27 bps from issuing floating rate debt directly. Firm B has effectively issued fixed rate

debt at 10.25 per cent saving 15 bps from issuing fixed rate debt directly. The intermediary reaps

28 bps: + 40 bps on the fixed rate debt and – 12 bps on the floating rate debt. Hence the total gain

from the swap to all parties is 70 bps.

9.4.4 Interest Rate Swaps – The Indian Scenario

Rupee derivatives – interest rate swaps and forward rate agreements – are now an integral part

of the domestic money and debt markets. However, to begin with, these products can be offered

as plain vanilla products only. One of the salient features of a generic or plain vanilla swap is

that the first leg remains fixed throughout the life of the swap deal but the second leg floats with

the chosen reference rate.

LOVELY PROFESSIONAL UNIVERSITY 149