Page 119 - DCOM206_COST_ACCOUNTING_II

P. 119

Cost Accounting – II

Notes The detailed discussion of classification of budgets is as follows:

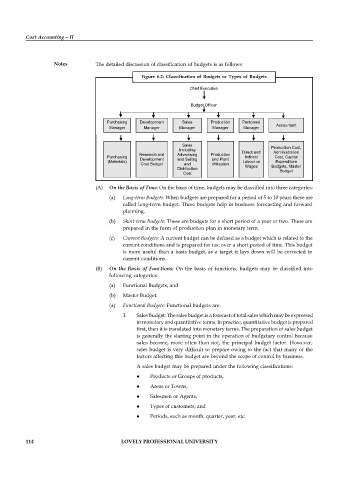

Figure 6.2: Classification of Budgets or Types of Budgets

Chief Executive

Budget Officer

Purchasing Development Sales Production Personnel

Accountant

Manager Manager Manager Manager Manager

Sales

Including Production Cost,

Research and Advertising Production Direct and Administration

Purchasing Development and Selling and Plant Indirect Cost, Capital

(Materials) Labour or Expenditure

Cost Budget and Utilization Wages Budgets, Master

Distribution Budget

Cost

(A) On the Basis of Time: On the basis of time, budgets may be classified into three categories:

(a) Long-term Budgets: When budgets are prepared for a period of 5 to 10 years these are

called long-term budget. These budgets help in business forecasting and forward

planning.

(b) Short-term Budgets: These are budgets for a short period of a year or two. These are

prepared in the form of production plan in monetary term.

(c) Current Budgets: A current budget can be defined as a budget which is related to the

current conditions and is prepared for use over a short period of time. This budget

is more useful than a basis budget, as a target it lays down will be corrected to

current conditions.

(B) On the Basis of Functions: On the basis of functions, budgets may be classified into

following categories:

(a) Functional Budgets, and

(b) Master Budget.

(a) Functional Budgets: Functional budgets are:

1. Sales Budget: The sales budget is a forecast of total sales which may be expressed

in monetary and quantitative terms. In practice, quantitative budget is prepared

first, then it is translated into monetary terms. The preparation of sales budget

is generally the starting point in the operation of budgetary control because

sales become, more often than not, the principal budget factor. However,

sales budget is very difficult to prepare owing to the fact that many of the

factors affecting this budget are beyond the scope of control by business.

A sales budget may be prepared under the following classifications:

Products or Groups of products,

Areas or Towns,

Salesmen or Agents,

Types of customers, and

Periods, such as month, quarter, year, etc.

114 LOVELY PROFESSIONAL UNIVERSITY