Page 195 - DCOM302_MANAGEMENT_ACCOUNTING

P. 195

Management Accounting

Notes 2. The price variance may be due to two courses of action, which are as follows:

(a) Cost effectiveness strategy and

(b) Distinctiveness Strategy.

Sales Volume Variance

It is one of the elements of sales variance, which is in between the actual sales quantity and

budgeted sales quantity. The variance is normally expressed in terms of price, i.e. standard price.

The purpose of expressing the variance in terms of standard price is that price which is free from

market forces.

Sales Volume Variance = Standard Price (Actual Quantity of Sale – Standard Quantity of

Sales)

The sales volume variance can be divided into two different streams that sales mix variance and

sales quantity variance/sub-usage variance.

1. Sales Mix Variance: It is the difference in between the actual sales and standard sales mix.

This variance will arise only due to change in the proportion of goods sold. This is a most

important variance usually computed/calculated, at the moment, the firm which deals

more than one commodity.

If both, the standard and actual mixes are equivalent to each other, there will not be any

mix variance in between the above mentioned.

If the mixes are totally different from each other, the sales mix variance is to be computed,

through the development of revised standard mix of quantities with reference to actual

quantities sold, then only the comparison will be meaningful to study the variances

occurred in between above mentioned. The sales mix variance is expressed in between

two different quantities and finally should be denominated in terms of standard price. The

reason for the expression in terms of standard price is the price which is totally free from

the demand and supply forces of the market.

Sales Mix Variance = Standard Price (Actual Quantity – Revised Standard Quantity)

2. Sale Sub-usage Variance: It is another component of usage variance, which expresses the

deviation in between the revised standard quantity to the tune of actual quantities sold and

the early set standard quantities expected to sell.

This variance also elucidates the differences of the above mentioned only in terms

of standard price, which is the ideal indicator free from the market forces i.e free from

fl uctuation.

Sales Sub-usage Variance = Standard Price (Revised Standard Quantity – Standard

Quantity).

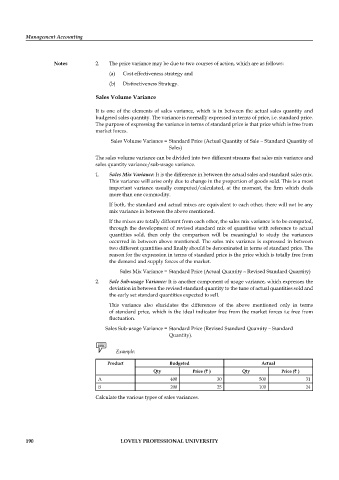

Example:

Product Budgeted Actual

Qty Price (` ) Qty Price (` )

A 400 30 500 31

B 200 25 100 24

Calculate the various types of sales variances.

190 LOVELY PROFESSIONAL UNIVERSITY