Page 221 - DCOM302_MANAGEMENT_ACCOUNTING

P. 221

Management Accounting

Notes 11.1 Absorption Costing

Absorption costing technique is also known by other names as “Full costing” or “Traditional

costing”. According to this technique, all costs are recognised or identified with the products

manufactured. Both fixed and variable costs of each product manufactured are taken into account

to ascertain the total cost.

According to author, the absorption costing tells as to how much fixed cost is absorbed besides

the variable cost by each product manufactured. According to this technique, while the variable

costs are directly charged to each unit of the goods produced, the fi xed costs are distributed to

each category of product manufactured by the same firm. In absorption costing, “Fixed cost” will

also be taken into account in ascertaining the profit on sale.

This technique is called traditional costing, as this system of costing emerged from the beginning

of the factory stage. In this technique, “fixed cost” refers to the closing stock of material held by

the firm. These are charged against the sales later, as a part of the goods sold.

The traditional technique popularly known as total cost or absorption costing technique does not

make any difference between fixed and variable cost in the calculation of profi t.

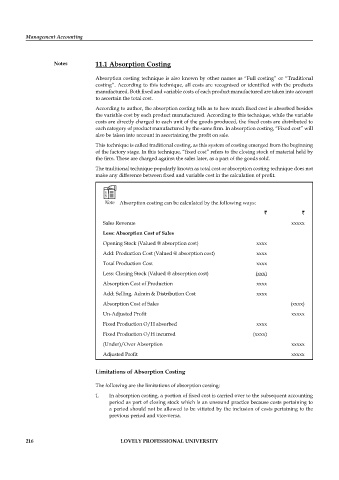

Note Absorption costing can be calculated by the following ways:

` `

Sales Revenue xxxxx

Less: Absorption Cost of Sales

Opening Stock (Valued @ absorption cost) xxxx

Add: Production Cost (Valued @ absorption cost) xxxx

Total Production Cost xxxx

Less: Closing Stock (Valued @ absorption cost) (xxx)

Absorption Cost of Production xxxx

Add: Selling, Admin & Distribution Cost xxxx

Absorption Cost of Sales (xxxx)

Un-Adjusted Profi t xxxxx

Fixed Production O/H absorbed xxxx

Fixed Production O/H incurred (xxxx)

(Under)/Over Absorption xxxxx

Adjusted Profi t xxxxx

Limitations of Absorption Costing

The following are the limitations of absorption costing:

1. In absorption costing, a portion of fixed cost is carried over to the subsequent accounting

period as part of closing stock which is an unsound practice because costs pertaining to

a period should not be allowed to be vitiated by the inclusion of costs pertaining to the

previous period and vice-versa.

216 LOVELY PROFESSIONAL UNIVERSITY