Page 237 - DCOM302_MANAGEMENT_ACCOUNTING

P. 237

Management Accounting

Notes (`)

Sales 20,00,000

Fixed Costs 5,00,000

Variable costs 12,00,000

Solution:

Total Contribution: (`)

Sales 20,00,000

Variable Cost 12,00,000

Contribution 8,00,000

As percentage of sales or P/V ratio = ` 8,00,000/` 20,00,000 × 100 = 40%

Alternatively: (Fixed Cost + Profit)/Sales × 100

(` 5,00,000 + ` 3,00,000/` 20,00,000) × 100 = 40%

Break-even sales:

Fixed Costs/P/V Ratio i.e., ` 5,00,000 × 100/40 = ` 12,50,000

Proof: Variable Costs: (`)

60% of ` 12,50,000 7,50,000

Fixed Costs 5,00,000

Total Cost 12,50,000

Total costs equal sales; hence there is neither profit nor loss.

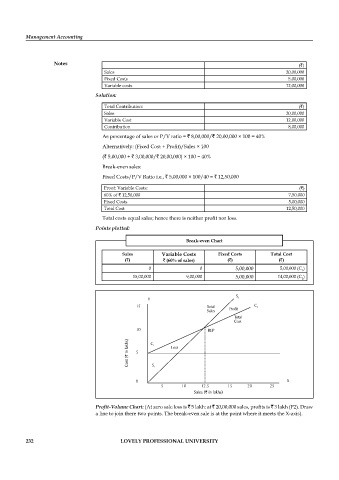

Points plotted:

Break-even Chart

Sales Variable Costs Fixed Costs Total Cost

(`) ` (60% of sales) (`) (`)

0 0 5,00,000 5,00,000 (C )

1

15,00,000 9,00,000 5,00,000 14,00,000 (C )

2

Y S 2

15 Total C 2

Sales Profit

Total

Cost

10 BEP

Cost (Rs. in lakhs) Cost (` in lakhs) 5 C 1 S 1 Loss

0 X

5 10 12.5 15 20 25

Sales (Rs. in lakhs)

Sales (` in lakhs)

Profi t-Volume Chart: (At zero sale loss is ` 5 lakh: at ` 20,00,000 sales, profi ts is ` 3 lakh (P2). Draw

a line to join there two points. The break-even sale is at the point where it meets the X-axis).

232 LOVELY PROFESSIONAL UNIVERSITY