Page 147 - DCOM302_MANAGEMENT_ACCOUNTING

P. 147

Management Accounting

Notes

Notes Utilities of the fl exible budget:

1. This budget is most useful tool of analysis in studying the sales at when the

circumstances are not warranting to predict.

2. It is mostly suited to the seasonal business, where the sales volume is getting differed

from one period to another due to changes taken place in the taste and preferences of

the buyers.

3. The production is being done on the basis of demand of the products in the market.

The demand of the products is studied only through demand forecasting. The

flexible budget is more applicable in the case of products, which are greatly fi nding

difficult to forecast the demand.

4. The budget is prepared only during the time of acute shortage of resources of

production viz. Men, Material and so on.

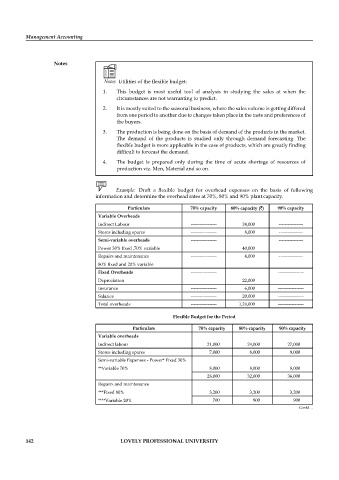

Example: Draft a flexible budget for overhead expenses on the basis of following

information and determine the overhead rates at 70%, 80% and 90% plant capacity.

Particulars 70% capacity 80% capacity (`) 90% capacity

Variable Overheads

Indirect Labour ----------------- 24,000 ----------------

Stores including spares ----------------- 8,000 ----------------

Semi-variable overheads ----------------- ----------------

Power 30% fixed ,70% variable 40,000

Repairs and maintenance ----------------- 4,000 ----------------

80% fixed and 20% variable

Fixed Overheads ----------------- -----------------

Depreciation 22,000

Insurance ----------------- 6,000 -----------------

Salaries ----------------- 20,000 -----------------

Total overheads ----------------- 1,24,000 -----------------

Flexible Budget for the Period

Particulars 70% capacity 80% capacity 90% capacity

Variable overheads

Indirect labour 21,000 24,000 27,000

Stores including spares 7,000 8,000 9,000

Semi-variable Expenses - Power* Fixed 30%

**Variable 70% 8,000 8,000 8,000

28,000 32,000 36,000

Repairs and maintenance

***Fixed 80% 3,200 3,200 3,200

****Variable 20% 700 800 900

Contd…

142 LOVELY PROFESSIONAL UNIVERSITY