Page 214 - DCOM302_MANAGEMENT_ACCOUNTING

P. 214

Unit 10: Responsibility Accounting and Transfer Pricing

Notes

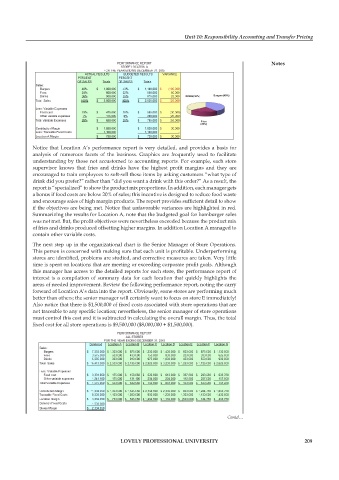

Notice that Location A’s performance report is very detailed, and provides a basis for

analysis of numerous facets of the business. Graphics are frequently used to facilitate

understanding by those not accustomed to accounting reports. For example, each store

supervisor knows that fries and drinks have the highest profit margins and they are

encouraged to train employees to soft-sell these items by asking customers “what type of

drink did you prefer?” rather than “did you want a drink with this order?” As a result, the

report is “specialized” to show the product mix proportions. In addition, each manager gets

a bonus if food costs are below 20% of sales; this incentive is designed to reduce food waste

and encourage sales of high margin products. The report provides sufficient detail to show

if the objectives are being met. Notice that unfavorable variances are highlighted in red.

Summarizing the results for Location A, note that the budgeted goal for hamburger sales

was not met. But, the profit objectives were nevertheless exceeded because the product mix

of fries and drinks produced offsetting higher margins. In addition Location A managed to

contain other variable costs.

The next step up in the organizational chart is the Senior Manager of Store Operations.

This person is concerned with making sure that each unit is profitable. Underperforming

stores are identified, problems are studied, and corrective measures are taken. Very little

time is spent on locations that are meeting or exceeding corporate profit goals. Although

this manager has access to the detailed reports for each store, the performance report of

interest is a compilation of summary data for each location that quickly highlights the

areas of needed improvement. Review the following performance report, noting the carry

forward of Location A’s data into the report. Obviously, some stores are performing much

better than others; the senior manager will certainly want to focus on store E immediately!

Also notice that there is $1,500,000 of fixed costs associated with store operations that are

not traceable to any specific location; nevertheless, the senior manager of store operations

must control this cost and it is subtracted in calculating the overall margin. Thus, the total

fixed cost for all store operations is $9,500,000 ($8,000,000 + $1,500,000).

Contd…

LOVELY PROFESSIONAL UNIVERSITY 209