Page 264 - DMGT405_FINANCIAL%20MANAGEMENT

P. 264

Financial Management

Notes The implication of relaxed credit standards is more credit, a larger credit department to service

accounts and related matters and increase in collection costs.

A relaxation in credit standard implies an increase in sales, which in turn, leads to higher

average accounts receivables. Further, relaxed standards would enable credit to get extended to

even less creditworthy customers, resulting in longer period to pay over dues. The reverse will

happen if credit standards are tightened.

Further, changing credit standards can also be expected to change the volume of sales. As

standards are relaxed, sales are expected to increase; conversely a tightening is expected to cause

a decline in sales.

!

Caution It must be kept in mind that with relaxation in credit standards, bad expenses will

go up.

The effect of alternative credit standards is illustrated in the following example:

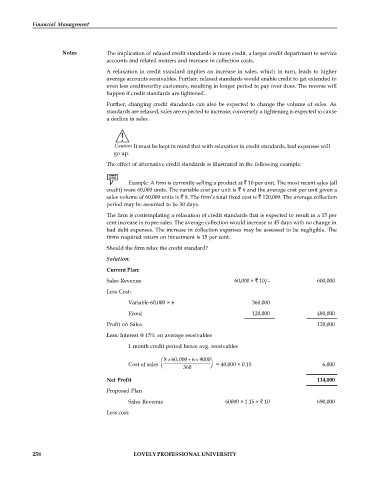

Example: A firm is currently selling a product at 10 per unit. The most recent sales (all

credit) were 60,000 units. The variable cost per unit is 6 and the average cost per unit given a

sales volume of 60,000 units is 8. The firm’s total fixed cost is 120,000. The average collection

period may be assumed to be 30 days.

The firm is contemplating a relaxation of credit standards that is expected to result in a 15 per

cent increase in rupee sales. The average collection would increase to 45 days with no change in

bad debt expenses. The increase in collection expenses may be assessed to be negligible. The

firms required return on investment is 15 per cent.

Should the firm relax the credit standard?

Solution:

Current Plan:

Sales Revenue 60,000 × 10/- 600,000

Less Cost:

Variable 60,000 × 6 360,000

Fixed 120,000 480,000

Profit on Sales 120,000

Less: Interest @ 15% on average receivables

1 month credit period hence avg. receivables

6

æ 8 ´ 60,000 + ´ 9000 ö

Cost of sales ç è 360 ÷ = 40,000 × 0.15 6,000

ø

Net Profit 114,000

Proposed Plan

Sales Revenue 60000 × 1.15 × 10 690,000

Less cost:

258 LOVELY PROFESSIONAL UNIVERSITY