Page 133 - DCOM409_CONTEMPORARY_ACCOUNTING

P. 133

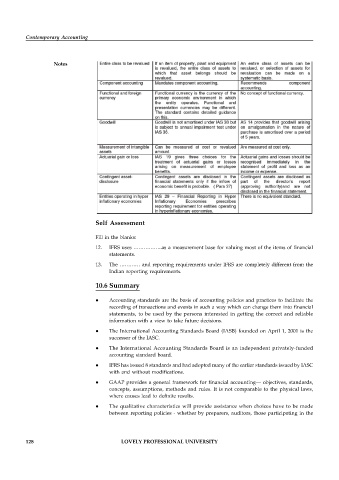

Contemporary Accounting

Notes

Self Assessment

Fill in the blanks:

12. IFRS uses ……………..as a measurement base for valuing most of the items of financial

statements.

13. The ………… and reporting requirements under IFRS are completely different from the

Indian reporting requirements.

10.6 Summary

Accounting standards are the basis of accounting policies and practices to facilitate the

recording of transactions and events in such a way which can change them into financial

statements, to be used by the persons interested in getting the correct and reliable

information with a view to take future decisions.

The International Accounting Standards Board (IASB) founded on April 1, 2001 is the

successor of the IASC.

The International Accounting Standards Board is an independent privately-funded

accounting standard board.

IFRS has issued 8 standards and had adopted many of the earlier standards issued by IASC

with and without modifications.

GAAP provides a general framework for financial accounting— objectives, standards,

concepts, assumptions, methods and rules. It is not comparable to the physical laws,

where causes lead to definite results.

The qualitative characteristics will provide assistance when choices have to be made

between reporting policies - whether by preparers, auditors, those participating in the

128 LOVELY PROFESSIONAL UNIVERSITY