Page 261 - DMGT202_COST_AND_MANAGEMENT_ACCOUNTING

P. 261

Cost and Management Accounting

Notes 14.2.1 The Basic Process

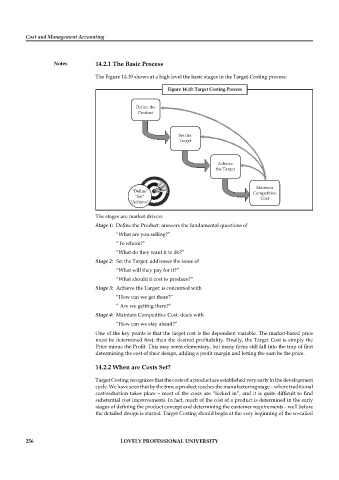

The Figure 14.10 shows at a high level the basic stages in the Target-Costing process:

Figure 14.10: Target Costing Process

Define the

Product

Set the

Target

Achieve

the Target

Maintain

"Define" Competitive

"Set" Cost

"Achieve"

The stages are market-driven:

Stage 1: Define the Product: answers the fundamental questions of

“What are you selling?”

“To whom?”

“What do they want it to do?”

Stage 2: Set the Target: addresses the issue of

“What will they pay for it?”

“What should it cost to produce?”

Stage 3: Achieve the Target: is concerned with

“How can we get there?”

“ Are we getting there?”

Stage 4: Maintain Competitive Cost: deals with

“How can we stay ahead?”

One of the key points is that the target cost is the dependent variable. The market-based price

must be determined first, then the desired profitability. Finally, the Target Cost is simply the

Price minus the Profit. This may seem elementary, but many firms still fall into the trap of fi rst

determining the cost of their design, adding a profit margin and letting the sum be the price.

14.2.2 When are Costs Set?

Target Costing recognizes that the costs of a product are established very early in the development

cycle. We have seen that by the time a product reaches the manufacturing stage – where traditional

cost-reduction takes place – most of the costs are “locked in”, and it is quite diffi cult to fi nd

substantial cost improvements. In fact, much of the cost of a product is determined in the early

stages of defining the product concept and determining the customer requirements - well before

the detailed design is started. Target Costing should begin at the very beginning of the so-called

256 LOVELY PROFESSIONAL UNIVERSITY