Page 263 - DMGT207_MANAGEMENT_OF_FINANCES

P. 263

Management of Finances

Notes 2. Maturity: Matching of maturing and forecasted cash needs is essential. Prices of long-

term securities fluctuate more with changes in interest rates and are therefore, more risky.

3. Marketability: It refers to the convenience, speed and cost at which a security can be

converted into cash. If the security can be sold quickly without loss of time and price, it is

highly liquid or marketable.

The choice of marketable securities is mainly limited to government treasury bills, deposits

with banks and inter-corporate deposits, units of Unit Trust of India and Commercial paper of

corporates are other attractive means of parking surplus funds for companies along with deposits

with sister concerns or associate companies.

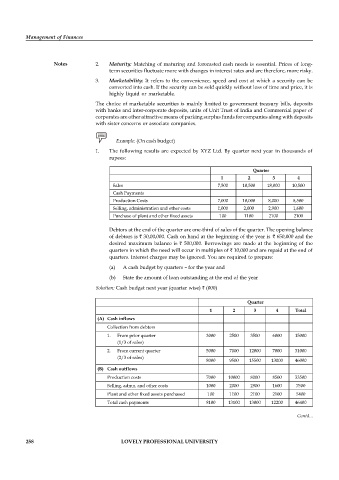

Example: (On cash budget)

1. The following results are expected by XYZ Ltd. By quarter next year in thousands of

rupees:

Quarter

1 2 3 4

Sales 7,500 10,500 18,000 10,500

Cash Payments

Production Costs 7,000 10,000 8,000 8,500

Selling, administration and other costs 1,000 2,000 2,900 1,600

Purchase of plant and other fixed assets 100 1100 2100 2100

Debtors at the end of the quarter are one-third of sales of the quarter. The opening balance

of debtors is 30,00,000. Cash on hand at the beginning of the year is 650,000 and the

desired maximum balance is 500,000. Borrowings are made at the beginning of the

quarters in which the need will occur in multiples of 10,000 and are repaid at the end of

quarters. Interest charges may be ignored. You are required to prepare:

(a) A cash budget by quarters – for the year and

(b) State the amount of loan outstanding at the end of the year

Solution: Cash budget next year (quarter wise) (000)

Quarter

1 2 3 4 Total

(A) Cash inflows

Collection from debtors

1. From prior quarter 3000 2500 3500 6000 15000

(1/3 of sales)

2. From current quarter 5000 7000 12000 7000 31000

(2/3 of sales)

8000 9500 15500 13000 46000

(B) Cash outflows

Production costs 7000 10000 8000 8500 33500

Selling, admn. and other costs 1000 2000 2900 1600 7500

Plant and other fixed assets purchased 100 1100 2100 2100 5400

Total cash payments 8100 13100 13000 12200 46400

(C) Surplus/(deficiency) (100) (3600) 2500 800 (400)

Contd...

Beginning balance 650 550 500 500 650

Ending balance (indicated) 550 (3050) 3000 1300 250

Borrowing required (deficiency 3550 3550

LOVELY PROFESSIONAL UNIVERSITY

258 + min. cash reqd.)

Repayment mode (balance – min. cash reqd.) (2500) (800) (3300)

Ending balance 550 500 500 500 500