Page 236 - DMGT514_MANAGEMENT_CONTROL_SYSTEMS

P. 236

Unit 12: Management Control for Differentiated Strategies

Notes

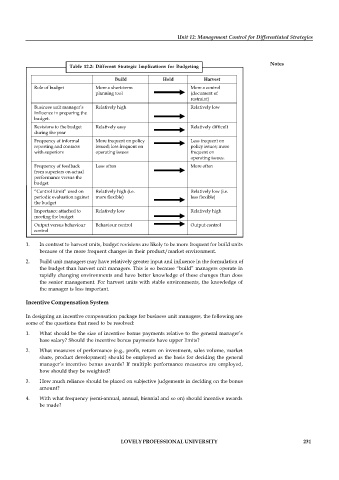

Table 12.2: Different Strategic Implications for Budgeting

Build Hold Harvest

Role of budget More a short-term More a control

planning tool (document of

restraint)

Business unit manager’s Relatively high Relatively low

Influence in preparing the

budget.

Revisions to the budget Relatively easy Relatively difficult

during the year

Frequency of informal More frequent on policy Less frequent on

reporting and contacts issued; less frequent on policy issues; more

with superiors operating issues frequent on

operating issues.

Frequency of feedback Less often More often

from superiors on actual

performance versus the

budget

“Control Limit” used on Relatively high (i.e. Relatively low (i.e.

periodic evaluation against more flexible) less flexible)

the budget

Importance attached to Relatively low Relatively high

meeting the budget

Output versus behaviour Behaviour control Output control

control

1. In contrast to harvest units, budget revisions are likely to be more frequent for build units

because of the more frequent changes in their product/market environment.

2. Build unit managers may have relatively greater input and influence in the formulation of

the budget than harvest unit managers. This is so because “build” managers operate in

rapidly changing environments and have better knowledge of these changes than does

the senior management. For harvest units with stable environments, the knowledge of

the manager is less important.

Incentive Compensation System

In designing an incentive compensation package for business unit managers, the following are

some of the questions that need to be resolved:

1. What should be the size of incentive bonus payments relative to the general manager’s

base salary? Should the incentive bonus payments have upper limits?

2. What measures of performance (e.g., profit, return on investment, sales volume, market

share, product development) should be employed as the basis for deciding the general

manager’s incentive bonus awards? If multiple performance measures are employed,

how should they be weighted?

3. How much reliance should be placed on subjective judgements in deciding on the bonus

amount?

4. With what frequency (semi-annual, annual, biennial and so on) should incentive awards

be made?

LOVELY PROFESSIONAL UNIVERSITY 231