Page 130 - DCOM201_ACCOUNTING_FOR_COMPANIES_I

P. 130

Unit 5: Redemption of Preference Shares

Working Note: Notes

1. Bank Balance = 3,00,000 + 2,00,000 + 2,10,000 – 4,40,000

= ` 2,70,000

2. Bonus shares can be issued by using the full amount of premium account.

Example 9: Redemption of Preference Shares by Fresh Issue of Equity Shares or by

Profits or by Both

Pass the necessary journal entries in the books of the company in connection with redeemable

preference shares in the following cases:

(i) A company issued 57,500 equity shares of ` 10 each, fully called up, for the redemption of

10,000; 8% Redeemable Preference Shares of ` 50 each at a premium of 15%.

(ii) For the redemption of 250, 10% preference shares of ` 200 each at a premium of 5%, a

company issued 5,000 equity shares of ` 10 each at 5% premium all payments on these

shares were duly received.

(iii) A company has to redeem 10% Redeemable Preference Shares of ` 5 lakhs using its profits

available for dividend.

(iv) For the payment of 5,000; 9% Redeemable Preference Shares of ` 100 each at a premium of

10%, a company issued 4,000 equity shares of ` 100 each at a premium of 10% and the

balance of the amount was paid out of profit. The full amount was received on this new

issue.

(v) For the redemption of 5,000; 7% Redeemable Preference Shares of ` 500 each, a company

issued 25,000 equity shares of ` 100 each at 10% discount and balance was payable from

profits.

(vi) For the redemption of 4,00; 7% Redeemable Preference Shares of ` 500 each at a premium

of 10%. The company utilised its profit.

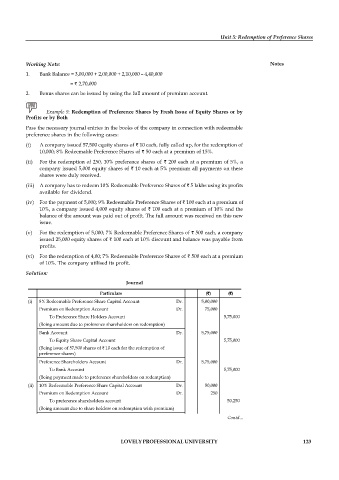

Solution:

Journal

Particulars (`) (`)

(i) 8% Redeemable Preference Share Capital Account Dr. 5,00,000

Premium on Redemption Account Dr. 75,000

To Preference Share Holders Account 5,75,000

(Being amount due to preference shareholders on redemption)

Bank Account Dr. 5,75,000

To Equity Share Capital Account 5,75,000

(Being issue of 57,500 shares of ` 10 each for the redemption of

preference shares)

Preference Shareholders Account Dr. 5,75,000

To Bank Account 5,75,000

(Being payment made to preference shareholders on redemption)

(ii) 10% Redeemable Preference Share Capital Account Dr. 50,000

Premium on Redemption Account Dr. 250

To preference shareholders account 50,250

(Being amount due to share holders on redemption with premium)

Share Premium Account Dr. 250 Contd...

To Premium on Redemption Account 250

(Being share premium utilised in writing off the premium on

redemption)

LOVELY PROFESSIONAL UNIVERSITY 123

Bank Account Dr. 50,250

To Equity Share Capital Account 50,000

To Share Premium Account 250

(Being receipt of amount from the issue of shares for redemption)

Preferences Shareholders Account Dr. 50,250

To Bank Account 50,250

(Being payment made to share holders on redemption)

(iii) 10% Redeemable Preference Share Capital Account Dr. 5,00,000

To Preference Shareholders Account 5,00,000

(Being amount due to shareholders on redemption of preference

shares)

Profit and Loss Account Dr. 5,00,000

To Capital Redemption Reserve A/c 5,00,000

(Being utilisation of profit for the redemption of preference shares)

Preference Shareholders Account Dr. 5,00,000

To Bank Account 5,00,000

(Being payment made to shareholders on redemption of preference

shares)

(iv) 9% Redeemable Preference Share Capital Account Dr. 5,00,000

Premium on Redemption Account Dr. 50,000

To Preference Share-holders Account 5,50,000

(Being amount due to share-holders on redemption of preference

shares)

Bank Account Dr. 4,40,000

To Equity Share Capital Account 4,00,000

To Share Premium Account 40,000

(Being receipt of amount from the issue of shares at premium)

Share Premium Account Dr. 40,000

Profit & Loss Account Dr. 10,000

To Premium on Redemption Account 50,000

(Being the utilisation of share premium and profit in writing off

premium on redemption)