Page 128 - DCOM201_ACCOUNTING_FOR_COMPANIES_I

P. 128

Unit 5: Redemption of Preference Shares

Amount of fresh issue of shares = 2,25,000 – 74,000 Notes

= 1,51,000

1,51,000

No. of shares to be issued = = 1,677.7 or 16,778

9

4. Bank balance = 1,01,500 + 1,51,002 + 45,000 – 2,55,000 = 42,502

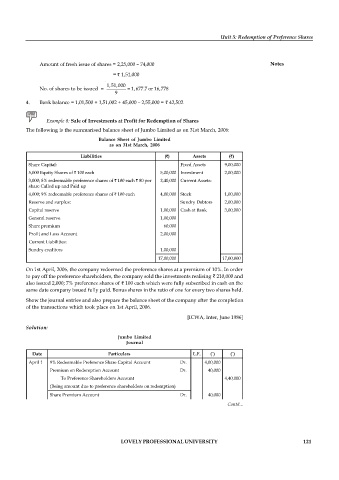

Example 8: Sale of Investments at Profit for Redemption of Shares

The following is the summarised balance sheet of Jumbo Limited as on 31st March, 2006:

Balance Sheet of Jumbo Limited

as on 31st March, 2006

Liabilities ( ) Assets ( )

Share Capital: Fixed Assets 9,00,000

5,000 Equity Shares of 100 each 5,00,000 Investment 2,00,000

3,000; 8% redeemable preference shares of 100 each 80 per 2,40,000 Current Assets:

share Called up and Paid up

4,000; 9% redeemable preference shares of 100 each 4,00,000 Stock 1,00,000

Reserve and surplus: Sundry Debtors 2,00,000

Capital reserve 1,00,000 Cash at Bank 3,00,000

General reserve 1,00,000

Share premium 60,000

Profit and Loss Account 2,00,000

Current Liabilities:

Sundry creditors 1,00,000

17,00,000 17,00,000

On 1st April, 2006, the company redeemed the preference shares at a premium of 10%. In order

to pay off the preference shareholders, the company sold the investments realising 210,000 and

also issued 2,000; 7% preference shares of 100 each which were fully subscribed in cash on the

same date company issued fully paid. Bonus shares in the ratio of one for every two shares held.

Show the journal entries and also prepare the balance sheet of the company after the completion

of the transactions which took place on 1st April, 2006.

[ICWA, Inter, June 1986]

Solution:

Jumbo Limited

Journal

Date Particulars L.F. (`) (`)

April 1 9% Redeemable Preference Share Capital Account Dr. 4,00,000

Premium on Redemption Account Dr. 40,000

To Preference Shareholders Account 4,40,000

(Being amount due to preference shareholders on redemption)

Share Premium Account Dr. 40,000

To Premium on Redemption Account Contd...

40,000

(Being utilisation of share premium in writing off the premium on

redemption)

General Reserve Account Dr. 1,00,000

Profit and Loss Account Dr. 1,00,000

LOVELY PROFESSIONAL UNIVERSITY 2,00,000

To Capital Redemption Reserve A/c 121

(Being the utilisation of general reserve and profits for redemption

of preference shares)

Bank Account Dr. 2,10,000

To Investment Account 2,00,000

To Profit and Loss Account 10,000

(Investments sold and profit transferred to P. & L. A/c)

Bank Account Dr. 2,00,000

To 7% Preference Share Capital Account 2,00,000

(Being receipt of amount on issue of 2,000 shares)

Preference Shareholders Account Dr. 4,40,000

To Bank Account 4,40,000

(Being amount paid off to preference shareholders on redemption)

Capital Redemption Reserve Account Dr. 2,00,000

Profit and Loss Account Dr. 50,000

To Bonus to Shareholders Account 2,50,000

(2,500 bonus shares declared to 5,000 existing equity shareholders)

Bonus to Shareholders Account Dr. 2,50,000

To Equity Share Capital Account 2,50,000

(Being bonus shares issued)