Page 126 - DCOM201_ACCOUNTING_FOR_COMPANIES_I

P. 126

Unit 5: Redemption of Preference Shares

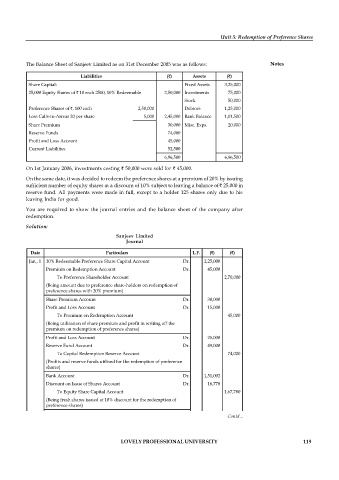

The Balance Sheet of Sanjeev Limited as on 31st December 2005 was as follows: Notes

Liabilities ( ) Assets ( )

Share Capital: Fixed Assets 3,25,000

25,000 Equity Shares of 10 each 2500, 10% Redeemable 2,50,000 Investments 75,000

Stock 50,000

Preference Shares of , 100 each 2,50,000 Debtors 1,25,000

Less Calls-in-Arrear 20 per share 5,000 2,45,000 Bank Balance 1,01,500

Share Premium 30,000 Misc. Exps. 20,000

Reserve Funds 74,000

Profit and Loss Account 45,000

Current Liabilities 52,500

6,96,500 6,96,500

On 1st January 2006, investments costing 50,000 were sold for 45,000.

On the same date, it was decided to redeem the preference shares at a premium of 20% by issuing

sufficient number of equity shares at a discount of 10% subject to leaving a balance of 25,000 in

reserve fund. All payments were made in full, except to a holder 125 shares only due to his

leaving India for good.

You are required to show the journal entries and the balance sheet of the company after

redemption.

Solution:

Sanjeev Limited

Journal

Date Particulars L.F. ( ) ( )

Jan., 1 10% Redeemable Preference Share Capital Account Dr. 2,25,000

Premium on Redemption Account Dr. 45,000

To Preference Shareholder Account 2,70,000

(Being amount due to preference share-holders on redemption of

preference shares with 20% premium)

Share Premium Account Dr. 30,000

Profit and Loss Account Dr. 15,000

To Premium on Redemption Account 45,000

(Being utilisation of share premium and profit in writing off the

premium on redemption of preference shares)

Profit and Loss Account Dr. 25,000

Reserve Fund Account Dr. 49,000

To Capital Redemption Reserve Account 74,000

(Profits and reserve funds utilised for the redemption of preference

shares)

Bank Account Dr. 1,51,002

Discount on Issue of Shares Account Dr. 16,778

To Equity Share Capital Account 1,67,780

(Being fresh shares issued at 10% discount for the redemption of

preference shares)

Bank Account Dr. 45,000

Contd...

Profit and Loss Account Dr. 5,000

To investments account 50,000

(Being sale of investment and loss transferred to P/L A/c)

LOVELY PROFESSIONAL UNIVERSITY 119

Preference Shareholders Account Dr. 2,55,000

To Bank Account 2,55,000

(Being the payment of 2,125 preference shareholders)