Page 122 - DCOM201_ACCOUNTING_FOR_COMPANIES_I

P. 122

Unit 5: Redemption of Preference Shares

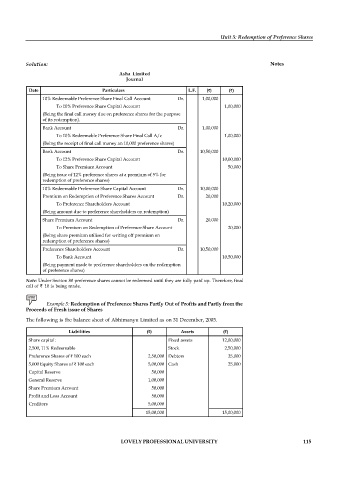

Solution: Notes

Asha Limited

Journal

Date Particulars L.F. ( ) ( )

10% Redeemable Preference Share Final Call Account Dr. 1,00,000

To 10% Preference Share Capital Account 1,00,000

(Being the final call money due on preference shares for the purpose

of its redemption).

Bank Account Dr. 1,00,000

To 10% Redeemable Preference Share Final Call A/c 1,00,000

(Being the receipt of final call money an 10,000 preference shares)

Bank Account Dr. 10,50,000

To 12% Preference Share Capital Account 10,00,000

To Share Premium Account 50,000

(Being issue of 12% preference shares at a premium of 5% for

redemption of preference shares)

10% Redeemable Preference Share Capital Account Dr. 10,00,000

Premium on Redemption of Preference Shares Account Dr. 20,000

To Preference Shareholders Account 10,20,000

(Being amount due to preference shareholders on redemption)

Share Premium Account Dr. 20,000

To Premium on Redemption of Preference Share Account 20,000

(Being share premium utilised for writing off premium on

redemption of preference shares)

Preference Shareholders Account Dr. 10,50,000

To Bank Account 10,50,000

(Being payment made to preference shareholders on the redemption

of preference shares)

Note: Under Section 80 preference shares cannot be redeemed until they are fully paid up. Therefore, final

call of 10 is being made.

Example 5: Redemption of Preference Shares Partly Out of Profits and Partly from the

Proceeds of Fresh issue of Shares

The following is the balance sheet of Abhimanyu Limited as on 31 December, 2005.

Liabilities ( ) Assets ( )

Share capital: Fixed assets 12,00,000

2,500, 11% Redeemable Stock 2,50,000

Preference Shares of 100 each 2,50,000 Debtors 25,000

5,000 Equity Shares of 100 each 5,00,000 Cash 25,000

Capital Reserve 50,000

General Reserve 1,00,000

Share Premium Account 50,000

Profit and Loss Account 50,000

Creditors 5,00,000

15,00,000 15,00,000

LOVELY PROFESSIONAL UNIVERSITY 115