Page 124 - DCOM201_ACCOUNTING_FOR_COMPANIES_I

P. 124

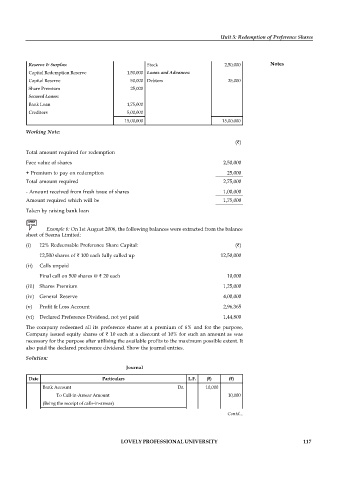

Liabilities ( ) Assets ( )

Unit 5: Redemption of Preference Shares

Share Capital: Fixed Assets: 12,00,000

6,000 Equity Shares of 100 Current Assets:

each fully paid up 6,00,000 Cash Balance 25,000

Reserve & Surplus: Stock 2,50,000 Notes

Capital Redemption Reserve 1,50,000 Loans and Advances:

Capital Reserve 50,000 Debtors 25,000

Share Premium 25,000

Secured Loans:

Bank Loan 1,75,000

Creditors 5,00,000

15,00,000 15,00,000

Working Note:

( )

Total amount required for redemption

Face value of shares 2,50,000

+ Premium to pay on redemption 25,000

Total amount required 2,75,000

- Amount received from fresh issue of shares 1,00,000

Amount required which will be 1,75,000

Taken by raising bank loan

Example 6: On 1st August 2006, the following balances were extracted from the balance

sheet of Seema Limited:

(i) 12% Redeemable Preference Share Capital: ( )

12,500 shares of 100 each fully called up 12,50,000

(ii) Calls unpaid

Final call on 500 shares @ 20 each 10,000

(iii) Shares Premium 1,25,000

(iv) General Reserve 4,00,000

(v) Profit & Loss Account 2,96,365

(vi) Declared Preference Dividend, not yet paid 1,44,800

The company redeemed all its preference shares at a premium of 6% and for the purpose,

Company issued equity shares of 10 each at a discount of 10% for such an amount as was

necessary for the purpose after utilising the available profits to the maximum possible extent. It

also paid the declared preference dividend. Show the journal entries.

Solution:

Journal

Date Particulars L.F. ( ) ( )

Bank Account Dr. 10,000

To Call-in-Arrear Amount 10,000

(Being the receipt of calls-in-arrear)

12% Redeemable Preference Share Capital Account Dr. 12,50,000 Contd...

Premium on Redemption Account Dr. 75,000

To Preference Shares-holders Account 13,25,000

(Being amount due to preferences shareholders on redemption of

preference share on premium) LOVELY PROFESSIONAL UNIVERSITY 117

General Reserve Account Dr. 4,00,000

Profit & Loss Account Dr. 2,96,365

To Capital Redemption Reserve A/c 6,96,365

(Being profit and general reserve utilised for redemption of

preference shares)

Share Premium Account Dr. 75,000

To Premium on Redemption Account 75,000

(Being the utilisation of share premium for writing off the premium

on redemption.)

Bank Account Dr. 5,53,680

Discount on Issue of Share Account Dr. 61,520

To Equity Shares Capital Account 6,15,200

(Being the receipt of the proceeds from the issue of 6,152 shares of

100 each at 10% discount.)

Preference Shares’ Dividend Account Dr. 1,44,800

To Bank Account 1,44,800

(Being payment made of declared preference dividend)

Preference Shareholders’ Account Dr. 13,25,000

To Bank Account 13,25,000

(Being payment made to preference shareholders on redemption)