Page 127 - DCOM201_ACCOUNTING_FOR_COMPANIES_I

P. 127

( )

Particulars

( )

Date

Dr.

45,000

Premium on Redemption Account

To Preference Shareholder Account

(Being amount due to preference share-holders on redemption of

preference shares with 20% premium)

30,000

Dr.

Share Premium Account

15,000

Dr.

Profit and Loss Account

45,000

To Premium on Redemption Account

(Being utilisation of share premium and profit in writing off the

premium on redemption of preference shares)

Profit and Loss Account

Dr.

25,000

49,000

Reserve Fund Account

Dr.

74,000

To Capital Redemption Reserve Account

Jan., 1 10% Redeemable Preferences Share Capital Account Dr. L.F. 2,25,000 2,70,000

(Profits and reserve funds utilised for the redemption of preference

shares)

Bank Account Dr. 1,51,002

Accounting for Companies-I Discount on Issue of Shares Account Dr. 16,778

To Equity Share Capital Account 1,67,780

(Being fresh shares issued at 10% discount for the redemption of

preference shares)

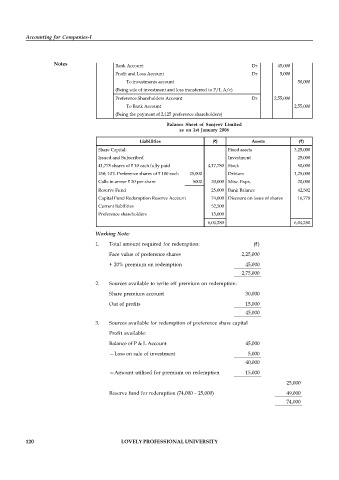

Notes Bank Account Dr. 45,000

Profit and Loss Account Dr. 5,000

To investments account 50,000

(Being sale of investment and loss transferred to P/L A/c)

Preference Shareholders Account Dr. 2,55,000

To Bank Account 2,55,000

(Being the payment of 2,125 preference shareholders)

Balance Sheet of Sanjeev Limited

as on 1st January 2006

Liabilities ( ) Assets ( )

Share Capital: Fixed assets 3,25,000

Issued and Subscribed Investment 25,000

41,778 shares of 10 each fully paid 4,17,780 Stock 50,000

250; 10% Preference shares of 100 each 25,000 Debtors 1,25,000

Calls in arrear 20 per share 5000 20,000 Misc. Exps. 20,000

Reserve Fund 25,000 Bank Balance 42,502

Capital Fund Redemption Reserve Account 74,000 Discount on issue of shares 16,778

Current liabilities 52,500

Preference shareholders 15,000

6,04,280 6,04,280

Working Note:

1. Total amount required for redemption: ( )

Face value of preference shares 2,25,000

+ 20% premium on redemption 45,000

2,75,000

2. Sources available to write off premium on redemption:

Share premium account 30,000

Out of profits 15,000

45,000

3. Sources available for redemption of preference share capital

Profit available:

Balance of P & L Account 45,000

—Loss on sale of investment 5,000

40,000

—Amount utilised for premium on redemption 15,000

25,000

Reserve fund for redemption (74,000 – 25,000) 49,000

74,000

120 LOVELY PROFESSIONAL UNIVERSITY