Page 184 - DCOM201_ACCOUNTING_FOR_COMPANIES_I

P. 184

Unit 8: Methods of Redemption–I

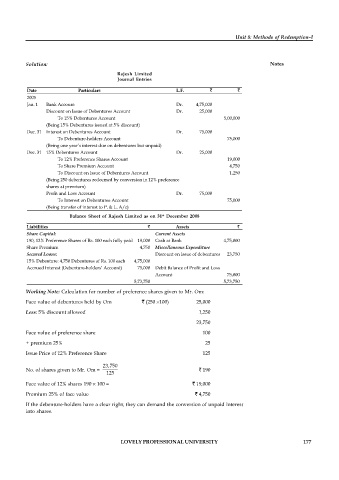

Solution: Notes

Rajesh Limited

Journal Entries

Date Particulars L.F. ` `

2005

Jan. 1 Bank Account Dr. 4,75,000

Discount on Issue of Debentures Account Dr. 25,000

To 15% Debentures Account 5,00,000

(Being 15% Debentures issued at 5% discount)

Dec. 31 Interest on Debentures Account Dr. 75,000

To Debenture-holders Account 75,000

(Being one year’s interest due on debentures but unpaid)

Dec. 31 15% Debentures Account Dr. 25,000

To 12% Preference Shares Account 19,000

To Share Premium Account 4,750

To Discount on Issue of Debentures Account 1,250

(Being 250 debentures redeemed by conversion in 12% preference

shares at premium)

Profit and Loss Account Dr. 75,000

To Interest on Debentures Account 75,000

(Being transfer of interest to P. & L. A/c)

st

Balance Sheet of Rajesh Limited as on 31 December 2008

Liabilities ` Assets `

Share Capital: Current Assets

190, 12% Preference Shares of Rs. 100 each fully paid 19,000 Cash at Bank 4,75,000

Share Premium 4,750 Miscellaneous Expenditure

Secured Loans: Discount on Issue of debentures 23,750

15% Debenture: 4,750 Debentures of Rs. 100 each 4,75,000

Accrued Interest (Debenture-holders’ Account) 75,000 Debit Balance of Profit and Loss

Account 75,000

5,73,750 5,73,750

Working Note: Calculation for number of preference shares given to Mr. Om:

Face value of debentures held by Om ` (250 100) 25,000

Less: 5% discount allowed 1,250

23,750

Face value of preference share 100

+ premium 25% 25

Issue Price of 12% Preference Share 125

23,750

No. of shares given to Mr. Om = ` 190

125

Face value of 12% shares 190 100 = ` 19,000

Premium 25% of face value ` 4,750

If the debenture-holders have a clear right, they can demand the conversion of unpaid interest

into shares.

LOVELY PROFESSIONAL UNIVERSITY 177