Page 262 - DCOM202_COST_ACCOUNTING_I

P. 262

Cost Accounting – I

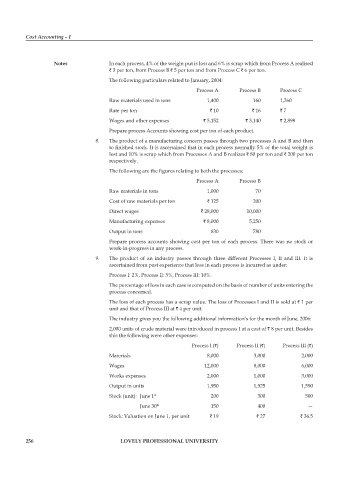

Notes In each process, 4% of the weight put is lost and 6% is scrap which from process A realised

` 3 per ton, from process B ` 5 per ton and from process C ` 6 per ton.

The following particulars related to January, 2004:

process A process B process C

Raw materials used in tons 1,400 160 1,260

Rate per ton ` 10 ` 16 ` 7

Wages and other expenses ` 5,152 ` 3,140 ` 2,898

prepare process Accounts showing cost per ton of each product.

8. The product of a manufacturing concern passes through two processes A and B and then

to finished stock. It is ascertained that in each process normally 5% of the total weight is

lost and 10% is scrap which from processes A and B realizes ` 80 per ton and ` 200 per ton

respectively.

The following are the figures relating to both the processes:

process A process B

Raw materials in tons 1,000 70

Cost of raw materials per ton ` 125 200

Direct wages ` 28,000 10,000

Manufacturing expenses ` 8,000 5,250

Output in tons 830 780

Prepare process accounts showing cost per ton of each process. There was no stock or

work-in-progress in any process.

9. The product of an industry passes through three different processes I, II and III. It is

ascertained from past experience that loss in each process is incurred as under:

process I: 2%, process II: 5%, process III: 10%.

The percentage of loss in each case is computed on the basis of number of units entering the

process concerned.

The loss of each process has a scrap value. The loss of processes I and II is sold at ` 1 per

unit and that of process III at ` 4 per unit.

The industry gives you the following additional information’s for the month of June, 2006:

2,000 units of crude material were introduced in process I at a cost of ` 8 per unit. Besides

this the following were other expenses:

process I (`) process II (`) process III (`)

Materials 8,000 3,000 2,000

Wages 12,000 8,000 6,000

Works expenses 2,000 1,000 3,000

Output in units 1,950 1,925 1,590

Stock (unit): June 1 200 300 500

st

June 30 150 400 —

th

Stock: Valuation on June 1, per unit ` 19 ` 27 ` 36.5

256 LOVELY PROFESSIONAL UNIVERSITY