Page 10 - DCOM205_ACCOUNTING_FOR_COMPANIES_II

P. 10

Unit 1: Acquisition of Business

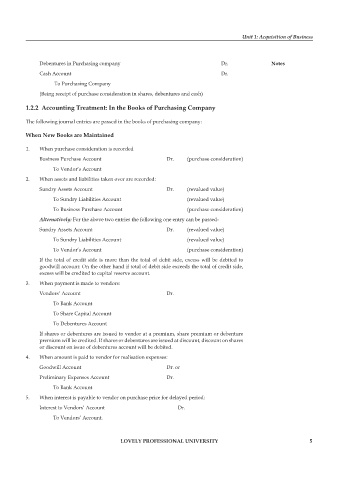

Debentures in Purchasing company Dr. notes

Cash Account Dr.

To Purchasing Company

(Being receipt of purchase consideration in shares, debentures and cash)

1.2.2 accounting treatment: in the Books of purchasing company

The following journal entries are passed in the books of purchasing company:

When new Books are maintained

1. When purchase consideration is recorded

Business Purchase Account Dr. (purchase consideration)

To Vendor’s Account

2. When assets and liabilities taken over are recorded:

Sundry Assets Account Dr. (revalued value)

To Sundry Liabilities Account (revalued value)

To Business Purchase Account (purchase consideration)

Alternatively: For the above two entries the following one entry can be passed-

Sundry Assets Account Dr. (revalued value)

To Sundry Liabilities Account (revalued value)

To Vendor’s Account (purchase consideration)

If the total of credit side is more than the total of debit side, excess will be debited to

goodwill account: On the other hand if total of debit side exceeds the total of credit side,

excess will be credited to capital reserve account.

3. When payment is made to vendors:

Vendors’ Account Dr.

To Bank Account

To Share Capital Account

To Debentures Account

If shares or debentures are issued to vendor at a premium, share premium or debenture

premium will be credited. If shares or debentures are issued at discount, discount on shares

or discount on issue of debentures account will be debited.

4. When amount is paid to vendor for realisation expenses:

Goodwill Account Dr. or

Preliminary Expenses Account Dr.

To Bank Account

5. When interest is payable to vendor on purchase price for delayed period:

Interest to Vendors’ Account Dr.

To Vendors’ Account.

lovely professional university 5