Page 21 - DCOM206_COST_ACCOUNTING_II

P. 21

(A) Earnings:

Income received (5,850 × 200)

11,70,000

11,70,000

(B) Fixed Charges: Particulars Total Amount (`)

Staff salaries : (4 × 800) + (6 × 500) + (4 × 300) × 12 88,800

Rent ( 30,000 × 12) 3,60,000

Repairs 16,000

Cost Accounting – II

Administration expenses 50,000

Cost of Oxygen, X-ray 65,000

Total 5,79,800

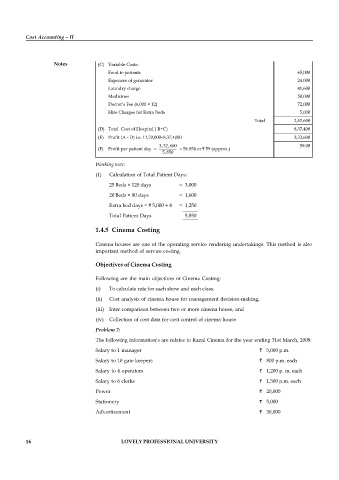

Notes (C) Variable Costs:

Food to patients 65,000

Expenses of generator 24,000

Laundry charge 41,600

Medicines 50,000

Doctor’s Fee (6,000 × 12) 72,000

Hire Charges for Extra Beds 5,000

Total 2,57,600

(D) Total Cost of Hospital ( B+C) 8,37,400

(E) Profit (A - D) i.e. 11,70,000–8,37,4000 3,32,600

3,32,600 59.00

(F) Profit per patient day = = 56.854 or ` 59 (approx.)

5,850

Working note:

(1) Calculation of Total Patient Days:

25 Beds × 120 days = 3,000

20 Beds × 80 days = 1,600

Extra bed days = ` 5,000 ÷ 4 = 1,250

Total Patient Days 5,850

1.4.5 Cinema Costing

Cinema houses are one of the operating service rendering undertakings. This method is also

important method of service costing.

Objectives of Cinema Costing

Following are the main objectives of Cinema Costing:

(i) To calculate rate for each show and each class,

(ii) Cost analysis of cinema house for management decision-making,

(iii) Inter comparison between two or more cinema house, and

(iv) Collection of cost data for cost control of cinema house.

Problem 7:

The following information’s are relates to Kazal Cinema for the year ending 31st March, 2008:

Salary to 1 manager ` 5,000 p.m.

Salary to 10 gate keepers ` 800 p.m. each

Salary to 4 operators ` 1,200 p. m. each

Salary to 6 clerks ` 1,500 p.m. each

Power ` 20,000

Stationery ` 5,000

Advertisement ` 30,000

16 LOVELY PROFESSIONAL UNIVERSITY