Page 158 - DCOM302_MANAGEMENT_ACCOUNTING

P. 158

Unit 8: Standard Costing

Standard costing is a system, which involves the various steps: Notes

1. The first step in implementing the standard costing system is to develop the pre-determined

standards, i.e., standard costs.

2. The second step is to record the actual costs through the ascertainment.

3. The third step involves with the comparison between the standards and actual costs;

which is the origin of the variance analysis. Standard costing starts with the preparation

of standards and ends with the comparison in between them. The preparation of standard

costs is meaningful only through the completion of variance analysis.

4. The fourth step is the stage at which the reasons for variances are probed and analysed to

incorporate the cost effectiveness not only to reduce cost but also to enhance the levels of

profit.

5. The final step is the most important in the organization to take managerial decisions

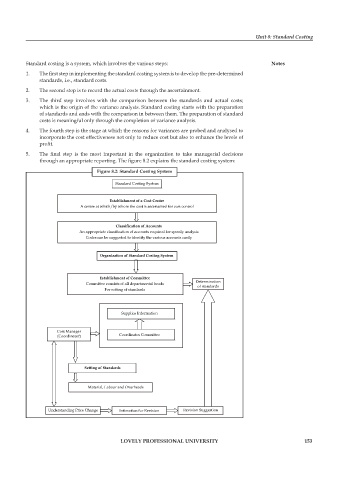

through an appropriate reporting. The figure 8.2 explains the standard costing system:

Figure 10.2

Figure 8.2: Standard Costing System

Standard Costing System

Establishment of a Cost Centre

A centre at which/by whom the cost is ascertained for cost control

Classification of Accounts

An appropriate classification of accounts required for speedy analysis

Codes can be suggested to identify the various accounts easily

Organization of Standard Costing System

Establishment of Committee

Committee consists of all departmental heads Determination

of standards

For setting of standards

Supplies Information

Cost Manager

(Coordinator) Coordinates Committee

Setting of Standards

Material, Labour and Overheads

Understanding Price Change Intimation for Revision Revision Suggestion

LOVELY PROFESSIONAL UNIVERSITY 153