Page 268 - DCOM302_MANAGEMENT_ACCOUNTING

P. 268

Unit 14: Management Reporting and MIS

Self Assessment Notes

State whether the following statements are true or false

6. Information that originates within an organisation is referred to as internal information.

7. The internal informations are essential for managing day-to-day operations.

8. External information is often required by top level managers to plan and guide the

organisation successfully.

9. Information means that data have been shaped into a form that is meaningful and useful to

human being.

14.3 Performance Measures

Performance measures are a central component of management information and reporting

system. This section deals with performance measures for different levels of an organization and

for managers at these levels – both financial and non-financial performance measures.

Performance measurements of an organisation unit should be a prerequisite for allocating

resources within that organisation. When a unit undertakes new activities projections of

revenues, costs and investments are made. An ongoing comparison of the actual revenues, costs

and investments with the budgeted amounts can help guide top management’s decisions about

future allocations.

Performance measurement of managers is used in decisions about their salaries, bonus, future

assignments and status, which motivate managers to strive for the goals used in their evaluation.

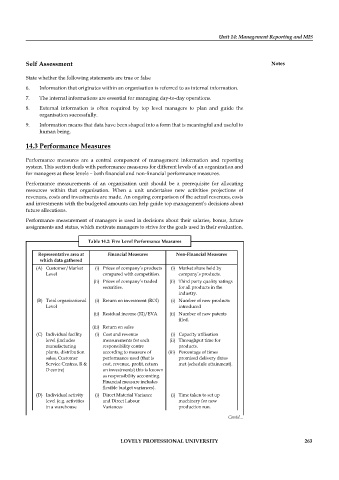

Table 14.2: Five Level Performance Measures

Representative area at Financial Measures Non-Financial Measures

which data gathered

(A) Customer/Market (i) Prices of company’s products (i) Market share held by

Level compared with competition. company’s products.

(ii) Prices of company’s traded (ii) Third party quality ratings

securities. for all products in the

industry.

(B) Total organisational (i) Return on investment (ROI) (i) Number of new products

Level introduced

(ii) Residual income (RI)/EVA (ii) Number of new patents

fi led.

(iii) Return on sales

(C) Individual facility (i) Cost and revenue (i) Capacity utilisation

level (includes measurements for each (ii) Throughput time for

manufacturing responsibility centre products.

plants, distribution according to measure of (iii) Percentage of times

sales, Customer performance used (that is promised delivery dates

Service Centres, R & cost, revenue, profi t, return met (schedule attainment).

D centre) on investments) this is known

as responsibility accounting.

Financial measure includes

flexible budget variances).

(D) Individual activity (i) Direct Material Variance (i) Time taken to set up

level (e.g. activities and Direct Labour machinery for new

in a warehouse Variances production run.

Contd...

LOVELY PROFESSIONAL UNIVERSITY 263