Page 183 - DECO405_MANAGERIAL_ECONOMICS

P. 183

Managerial Economics

Notes 11.2 Price and Output Decisions

Long Run Equilibrium through New Entry Competition

Under monopolistic competition, the number of independent firms selling differentiated products

or brands of a given commodity is large and the relative market share of every firm is

insignificant. Therefore, the entry of a new firm into the market will not have any noticeable

adverse effect on the sales (or demand) of any of the established firms. Established firms will

have no reason to react to new entry by adopting practices to discourage this. Moreover, there

are no legal or non-legal (economic) barriers against new entry. Hence, when high profits of the

existing firms attract new entry, new firms will in fact enter the market.

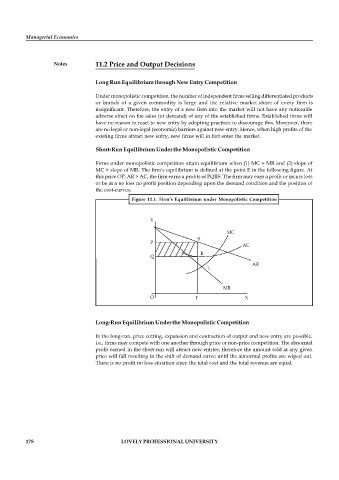

Short-Run Equilibrium Under the Monopolistic Competition

Firms under monopolistic competition attain equilibrium when (1) MC = MR and (2) slope of

MC > slope of MR. The firm's equilibrium is defined at the point E in the following figure. At

this price OP, AR > AC, the firm earns a profits of PQRS. The firm may earn a profit or incurs loss

or be at a no loss no profit position depending upon the demand condition and the position of

the cost-curves;

Figure 11.1: Firm’s Equilibrium under Monopolistic Competition

Long-Run Equilibrium Under the Monopolistic Competition

In the long-run, price cutting, expansion and contraction of output and new entry are possible,

i.e., firms may compete with one another through price or non-price competition. The abnormal

profit earned in the short-run will attract new entries, therefore the amount sold at any given

price will fall resulting in the shift of demand curve until the abnormal profits are wiped out.

There is no profit no loss situation since the total cost and the total revenue are equal.

178 LOVELY PROFESSIONAL UNIVERSITY