Page 182 - DMGT104_FINANCIAL_ACCOUNTING

P. 182

( )

( )

Stock on 1.1.2007: Particulars Amount Amount

Raw Materials: 8,000 ---

Work-in-Progress 20,000 ---

Finished Goods 40,000 ---

Manufacturing Wages 40,000 ---

Financial Accounting

Purchases of Raw Materials 1,20,000 ---

Factory Rent 20,000 ---

Carriage of Raw Materials 12,000 ---

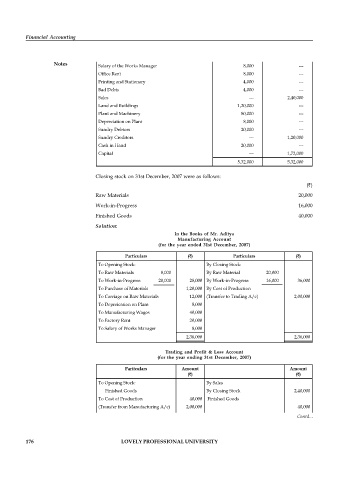

Notes Salary of the Works Manager 8,000 ---

Office Rent 8,000 ---

Printing and Stationary 4,000 ---

Bad Debts 4,000 ---

Sales --- 2,40,000

Land and Buildings 1,20,000 ---

Plant and Machinery 80,000 ---

Depreciation on Plant 8,000 ---

Sundry Debtors 20,000 ---

Sundry Creditors --- 1,20,000

Cash in Hand 20,000 ---

Capital --- 1,72,000

5,32,000 5,32,000

Closing stock on 31st December, 2007 were as follows:

( )

Raw Materials 20,000

Work-in-Progress 16,000

Finished Goods 40,000

Solution:

In the Books of Mr. Aditya

Manufacturing Account

(for the year ended 31st December, 2007)

Particulars ( ) Particulars ( )

To Opening Stock: By Closing Stock:

To Raw Materials 8,000 By Raw Material 20,000

To Work-in-Progress 20,000 28,000 By Work-in-Progress 16,000 36,000

To Purchase of Materials 1,20,000 By Cost of Production

To Carriage on Raw Materials 12,000 (Transfer to Trading A/c) 2,00,000

To Depreication on Plant 8,000

To Manufacturing Wages 40,000

To Factory Rent 20,000

To Salary of Works Manager 8,000

2,36,000 2,36,000

Trading and Profit & Loss Account

(for the year ending 31st December, 2007)

Particulars Amount Amount

( ) ( )

To Opening Stock: By Sales

Finished Goods By Closing Stock 2,40,000

To Cost of Production 40,000 Finished Goods

(Transfer from Manufacturing A/c) 2,00,000 40,000

To Gross Profit Contd...

(carried to P. & L. A/c)

40,000

2,80,000 By Gross Profit 2,80,000

176 LOVELY PROFESSIONAL UNIVERSITY

To Office Rent 8,000 (brought from Trading A/c)

To Printing & Stationary 4,000 40,000

To Bad Debts 4,000

To Net Profit (carried to Capital A/c)

24,000

40,000 40,000