Page 189 - DMGT104_FINANCIAL_ACCOUNTING

P. 189

Unit 8: Financial Statements

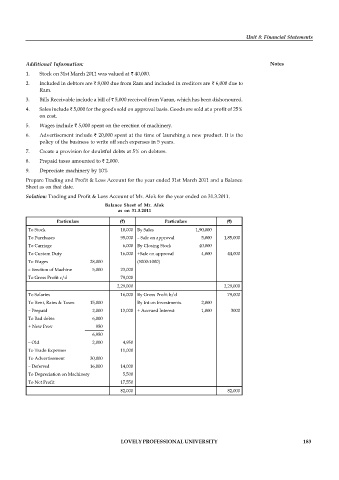

Additional Information: Notes

1. Stock on 31st March 2011 was valued at 40,000.

2. Included in debtors are 8,000 due from Ram and included in creditors are 6,000 due to

Ram.

3. Bills Receivable include a bill of 5,000 received from Varun, which has been dishonoured.

4. Sales include 5,000 for the goods sold on approval basis. Goods are sold at a profit of 25%

on cost.

5. Wages include 5,000 spent on the erection of machinery.

6. Advertisement include 20,000 spent at the time of launching a new product. It is the

policy of the business to write off such expenses in 5 years.

7. Create a provision for doubtful debts at 5% on debtors.

8. Prepaid taxes amounted to 2,000.

9. Depreciate machinery by 10%

Prepare Trading and Profit & Loss Account for the year ended 31st March 2011 and a Balance

Sheet as on that date.

Solution: Trading and Profit & Loss Account of Mr. Alok for the year ended on 31.3.2011.

Balance Sheet of Mr. Alok

as on 31.3.2011

Particulars ( ) Particulars ( )

To Stock 10,000 By Sales 1,90,000

To Purchases 95,000 – Sale on approval 5,000 1,85,000

To Carriage 6,000 By Closing Stock 40,000

To Custom Duty 16,000 +Sale on approval 4,000 44,000

To Wages 28,000 (5000-1000)

– Erection of Machine 5,000 23,000

To Gross Profit c/d 79,000

2,29,000 2,29,000

To Salaries 16,000 By Gross Profit b/d 79,000

To Rent, Rates & Taxes 15,000 By Int on Investments 2,000

– Prepaid 2,000 13,000 + Accrued Interest 1,000 3000

To Bad debts 6,000

+ New Prov 950

6,950

– Old 2,000 4,950

To Trade Expenses 11,000

To Advertisement 30,000

– Deferred 16,000 14,000

To Depreciation on Machinery 5,500

To Net Profit 17,550

82,000 82,000

LOVELY PROFESSIONAL UNIVERSITY 183