Page 105 - DMGT403_ACCOUNTING_FOR_MANAGERS

P. 105

Accounting for Managers

Notes 5.3 Elements of Cost

To find the total cost of the product or service, the costs incurred are grouped under various

categories.

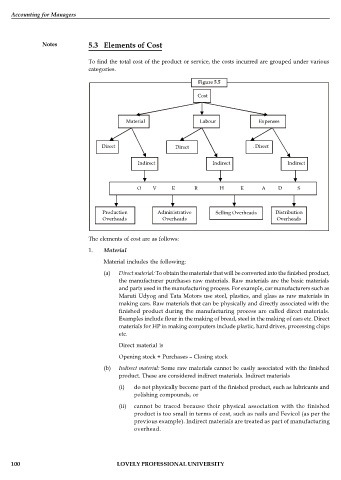

Figure 5.5

Cost

Material Labour Expenses

Direct Direct . Direct

Indirect Indirect Indirect

O V E R H E A D S

Production Administrative Selling Overheads Distribution

Overheads Overheads Overheads

The elements of cost are as follows:

1. Material

Material includes the following:

(a) Direct material: To obtain the materials that will be converted into the finished product,

the manufacturer purchases raw materials. Raw materials are the basic materials

and parts used in the manufacturing process. For example, car manufacturers such as

Maruti Udyog and Tata Motors use steel, plastics, and glass as raw materials in

making cars. Raw materials that can be physically and directly associated with the

finished product during the manufacturing process are called direct materials.

Examples include flour in the making of bread, steel in the making of cars etc. Direct

materials for HP in making computers include plastic, hard drives, processing chips

etc.

Direct material is

Opening stock + Purchases – Closing stock

(b) Indirect material: Some raw materials cannot be easily associated with the finished

product. These are considered indirect materials. Indirect materials

(i) do not physically become part of the finished product, such as lubricants and

polishing compounds, or

(ii) cannot be traced because their physical association with the finished

product is too small in terms of cost, such as nails and Fevicol (as per the

previous example). Indirect materials are treated as part of manufacturing

overhead.

100 LOVELY PROFESSIONAL UNIVERSITY