Page 152 - DCOM101_FINANCIAL_ACCOUNTING_I

P. 152

Financial Accounting-I

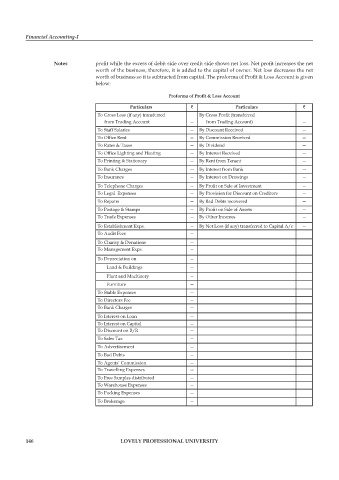

Notes profit while the excess of debit side over credit side shows net loss. Net profit increases the net

worth of the business, therefore, it is added to the capital of owner. Net loss decreases the net

worth of business so it is subtracted from capital. The proforma of Profit & Loss Account is given

below:

Proforma of Profit & Loss Account

Particulars ` Particulars `

To Gross Loss (if any) transferred By Gross Profi t (transferred

from Trading Account — from Trading Account) —

To Staff Salaries — By Discount Received —

To Office Rent — By Commission Received —

To Rates & Taxes — By Dividend —

To Office Lighting and Heating — By Interest Received —

To Printing & Stationary — By Rent from Tenant —

To Bank Charges — By Interest from Bank —

To Insurance — By Interest on Drawings —

To Telephone Charges — By Profit on Sale of Investment —

To Legal Expenses — By Provision for Discount on Creditors —

To Repairs — By Bad Debts recovered —

To Postage & Stamps — By Profit on Sale of Assets —

To Trade Expenses — By Other Incomes —

To Establishment Exps. — By Net Loss (if any) transferred to Capital A/c —

To Audit Fees —

To Charity & Donations —

To Management Exps. —

To Depreciation on —

Land & Buildings —

Plant and Machinery —

Furniture —

To Stable Expenses —

To Directors Fee —

To Bank Charges —

To Interest on Loan —

To Interest on Capital —

To Discount on B/R —

To Sales Tax —

To Advertisement —

To Bad Debts —

To Agents’ Commission —

To Travelling Expenses —

To Free Samples distributed —

To Warehouse Expenses —

To Packing Expenses —

To Brokerage —

146 LOVELY PROFESSIONAL UNIVERSITY