Page 177 - DCOM101_FINANCIAL_ACCOUNTING_I

P. 177

Unit 13: Bank Reconciliation Statement

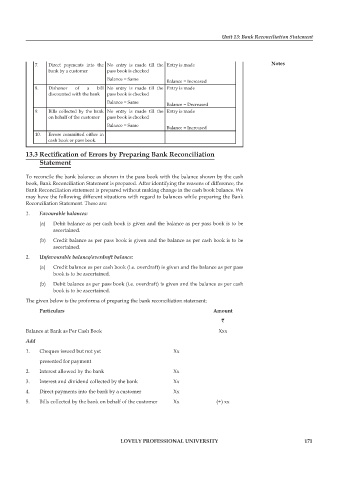

7. Direct payments into the No entry is made till the Entry is made Notes

bank by a customer pass book is checked

Balance = Same

Balance = Increased

8. Dishonor of a bill No entry is made till the Entry is made

discounted with the bank pass book is checked

Balance = Same

Balance = Decreased

9. Bills collected by the bank No entry is made till the Entry is made

on behalf of the customer pass book is checked

Balance = Same Balance = Increased

10. Errors committed either in

cash book or pass book.

13.3 Rectification of Errors by Preparing Bank Reconciliation

Statement

To reconcile the bank balance as shown in the pass book with the balance shown by the cash

book, Bank Reconciliation Statement is prepared. After identifying the reasons of difference, the

Bank Reconciliation statement is prepared without making change in the cash book balance. We

may have the following different situations with regard to balances while preparing the Bank

Reconciliation Statement. These are:

1. Favourable balances:

(a) Debit balance as per cash book is given and the balance as per pass book is to be

ascertained.

(b) Credit balance as per pass book is given and the balance as per cash book is to be

ascertained.

2. Unfavourable balance/overdraft balance:

(a) Credit balance as per cash book (i.e. overdraft) is given and the balance as per pass

book is to be ascertained.

(b) Debit balance as per pass book (i.e. overdraft) is given and the balance as per cash

book is to be ascertained.

The given below is the proforma of preparing the bank reconciliation statement:

Particulars Amount

`

Balance at Bank as Per Cash Book Xxx

Add

1. Cheques issued but not yet Xx

presented for payment

2. Interest allowed by the bank Xx

3. Interest and dividend collected by the bank Xx

4. Direct payments into the bank by a customer Xx

5. Bills collected by the bank on behalf of the customer Xx (+) xx

LOVELY PROFESSIONAL UNIVERSITY 171