Page 252 - DCOM202_COST_ACCOUNTING_I

P. 252

Cost Accounting – I

Notes in closing inventory and to obtain the net realized profit for a period, three columns have to be

shown in the ledger for showing the cost, unrealized profit and the transfer price.

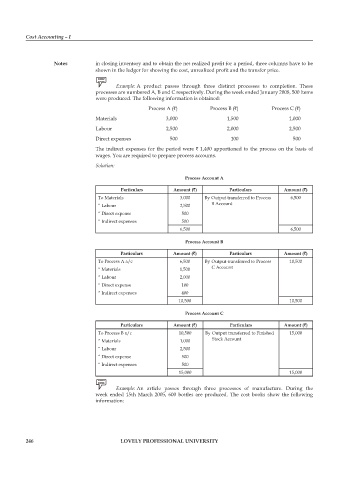

Example: A product passes through three distinct processes to completion. These

processes are numbered A, B and C respectively. During the week ended January 2008, 500 items

were produced. The following information is obtained:

process A (`) process B (`) process C (`)

Materials 3,000 1,500 1,000

Labour 2,500 2,000 2,500

Direct expenses 500 100 500

The indirect expenses for the period were ` 1,400 apportioned to the process on the basis of

wages. You are required to prepare process accounts.

Solution:

Process Account A

Particulars Amount (`) Particulars Amount (`)

To Materials 3,000 By Output transferred to process 6,500

“ Labour 2,500 B Account

“ Direct expense 500

“ Indirect expenses 500

6,500 6,500

Process Account B

Particulars Amount (`) Particulars Amount (`)

To process A a/c 6,500 By Output transferred to process 10,500

“ Materials 1,500 C Account

“ Labour 2,000

“ Direct expense 100

“ Indirect expenses 400

10,500 10,500

Process Account C

Particulars Amount (`) Particulars Amount (`)

To process B a/c 10,500 By Output transferred to Finished 15,000

“ Materials 1,000 Stock Account

“ Labour 2,500

“ Direct expense 500

“ Indirect expenses 500

15,000 15,000

Example: An article passes through three processes of manufacture. During the

week ended 15th March 2005, 600 bottles are produced. The cost books show the following

information:

246 LOVELY PROFESSIONAL UNIVERSITY