Page 277 - DCOM202_COST_ACCOUNTING_I

P. 277

Unit 13: Normal Wastage, Abnormal Loss and Abnormal Gain

13.6 Keywords Notes

Abnormal Gain: Gain out of abnormal effective usage

Crushing: pressing or Squeezing

Distinct Processes: Distinguishable

Oil Refinery: Refinery for petroleum

Production Techniques: Methods of production

13.7 Review Questions

1. Write short notes on abnormal gain or abnormal effective in process costing.

2. How would you account for wastage in the cost of production? Define normal wastage and

abnormal effective and distinguish between them.

3. Write short notes on:

(a) Scrap and wastage (b) Inter-Process Profit

(c) Joint Expenses (d) Equivalent production.

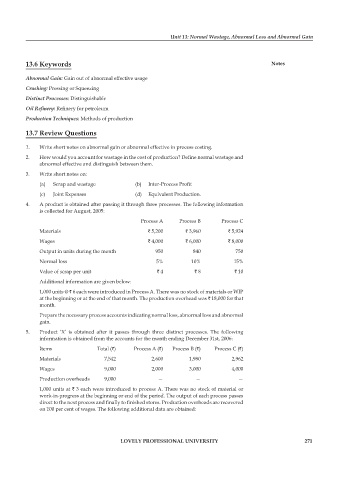

4. A product is obtained after passing it through three processes. The following information

is collected for August, 2005:

process A process B process C

Materials ` 5,200 ` 3,960 ` 5,924

Wages ` 4,000 ` 6,000 ` 8,000

Output in units during the month 950 840 750

Normal loss 5% 10% 15%

Value of scrap per unit ` 4 ` 8 ` 10

Additional information are given below:

1,000 units @ ` 6 each were introduced in Process A. There was no stock of materials or WIP

at the beginning or at the end of that month. The production overhead was ` 18,000 for that

month.

prepare the necessary process accounts indicating normal loss, abnormal loss and abnormal

gain.

5. Product ‘X’ is obtained after it passes through three distinct processes. The following

information is obtained from the accounts for the month ending December 31st, 2006:

Items Total (`) process A (`) process B (`) process C (`)

Materials 7,542 2,600 1,980 2,962

Wages 9,000 2,000 3,000 4,000

production overheads 9,000 — — —

1,000 units at ` 3 each were introduced to process A. There was no stock of material or

work-in-progress at the beginning or end of the period. The output of each process passes

direct to the next process and finally to finished stores. Production overheads are recovered

on 100 per cent of wages. The following additional data are obtained:

LOVELY PROFESSIONAL UNIVERSITY 271