Page 286 - DCOM202_COST_ACCOUNTING_I

P. 286

Cost Accounting – I

Notes Solution:

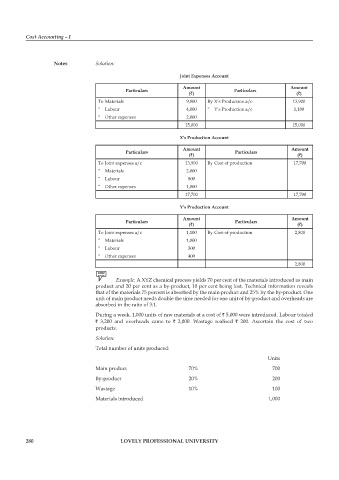

Joint Expenses Account

Amount Amount

Particulars Particulars

(`) (`)

To Materials 9,000 By X’s production a/c 13,900

“ Labour 4,000 “ Y’s Production a/c 1,100

“ Other expenses 2,000

15,000 15,000

X’s Production Account

Amount Amount

Particulars Particulars

(`) (`)

To Joint expenses a/c 13,900 By Cost of production 17,700

“ Materials 2,000

“ Labour 800

“ Other expenses 1,000

17,700 17,700

Y’s Production Account

Amount Amount

Particulars Particulars

(`) (`)

To Joint expenses a/c 1,100 By Cost of production 2,800

“ Materials 1,000

“ Labour 300

“ Other expenses 400

2,800

Example: A XYZ chemical process yields 70 per cent of the materials introduced as main

product and 20 per cent as a by-product, 10 per cent being lost. Technical information reveals

that of the materials 75 percent is absorbed by the main product and 25% by the by-product. One

unit of main product needs double the time needed for one unit of by-product and overheads are

absorbed in the ratio of 3:1.

During a week, 1,000 units of raw materials at a cost of ` 5,000 were introduced. Labour totaled

` 3,200 and overheads came to ` 2,000. Wastage realised ` 200. Ascertain the cost of two

products.

Solution:

Total number of units produced:

Units

Main product 70% 700

By-product 20% 200

Wastage 10% 100

Materials introduced 1,000

280 LOVELY PROFESSIONAL UNIVERSITY