Page 277 - DCOM205_ACCOUNTING_FOR_COMPANIES_II

P. 277

Accounting for Companies – II

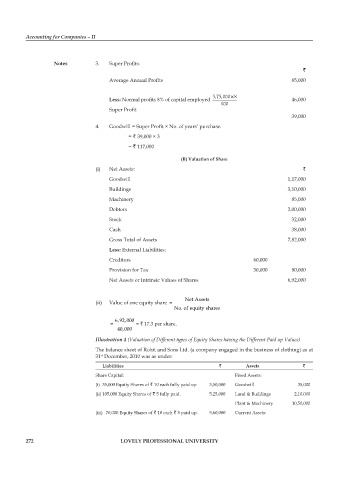

Notes 3. Super Profits:

`

Average Annual Profits 85,000

Less: Normal profits 8% of capital employed 5,75,000 ×8 46,000

100

Super Profit

39,000

4. Goodwill = Super Profit × No. of years’ purchase.

= ` 39,000 × 3

= ` 117,000

(B) Valuation of Share

(i) Net Assets: `

Goodwill 1,17,000

Buildings 3,10,000

Machinery 85,000

Debtors 2,00,000

Stock 32,000

Cash 38,000

Gross Total of Assets 7,82,000

Less: External Liabilities:

Creditors 60,000

Provision for Tax 30,000 90,000

Net Assets or Intrinsic Values of Shares 6,92,000

Net Assets

(ii) Value of one equity share =

No. of equity shares

6,92,000

= = ` 17.3 per share.

40,000

Illustration 4 (valuation of Different types of Equity Shares having the Different Paid up values)

The balance sheet of Rohit and Sons Ltd. (a company engaged in the business of clothing) as at

31 December, 2010 was as under:

st

Liabilities ` Assets `

Share Capital: Fixed Assets:

(i) 35,000 Equity Shares of ` 10 each fully paid up 3,50,000 Goodwill 35,000

(ii) 105,000 Equity Shares of ` 5 fully paid. 5,25,000 Land & Buildings 2,10,000

Plant & Machinery 10,50,000

(iii) 70,000 Equity Shares of ` 10 each ` 8 paid up. 5,60,000 Current Assets:

272 LOVELY PROFESSIONAL UNIVERSITY