Page 304 - DCOM205_ACCOUNTING_FOR_COMPANIES_II

P. 304

Unit 13: Valuation of Preference Shares

Notes

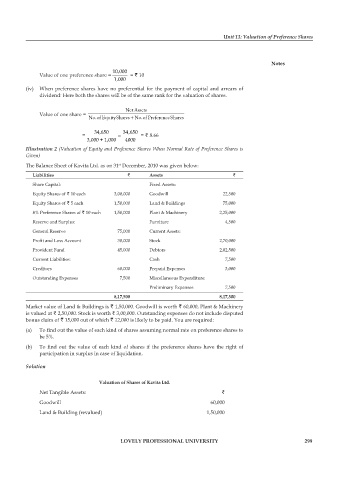

10,000

Value of one preference share = = ` 10

1,000

(iv) When preference shares have no preferential for the payment of capital and arrears of

dividend: Here both the shares will be of the same rank for the valuation of shares.

Net Assets

Value of one share =

+

No.of EquityShares No.of PreferenceShares

34,650 34,650

= = = ` 8.66

3,000 + 1,000 4000

Illustration 2 (Valuation of Equity and Preference Shares When Normal Rate of Preference Shares is

Given)

The Balance Sheet of Kavita Ltd. as on 31 December, 2010 was given below:

st

Liabilities ` Assets `

Share Capital: Fixed Assets:

Equity Shares of ` 10 each 3,00,000 Goodwill 22,500

Equity Shares of ` 5 each 1,50,000 Land & Buildings 75,000

8% Preference Shares of ` 10 each 1,50,000 Plant & Machinery 2,25,000

Reserve and Surplus: Furniture 4,500

General Reserve 75,000 Current Assets:

Profit and Loss Account 30,000 Stock 2,70,000

Provident Fund 45,000 Debtors 2,02,500

Current Liabilities: Cash 7,500

Creditors 60,000 Prepaid Expenses 3,000

Outstanding Expenses 7,500 Miscellaneous Expenditure:

Preliminary Expanses 7,500

8,17,500 8,17,500

Market value of Land & Buildings is ` 1,50,000. Goodwill is worth ` 60,000, Plant & Machinery

is valued at ` 2,50,000. Stock is worth ` 3,00,000. Outstanding expenses do not include disputed

bonus claim of ` 15,000 out of which ` 12,000 is likely to be paid. You are required:

(a) To find out the value of each kind of shares assuming normal rate on preference shares to

be 5%.

(b) To find out the value of each kind of shares if the preference shares have the right of

participation in surplus in case of liquidation.

Solution

Valuation of Shares of Kavita Ltd.

Net Tangible Assets: `

Goodwill 60,000

Land & Building (revalued) 1,50,000

LOVELY PROFESSIONAL UNIVERSITY 299