Page 222 - DCOM206_COST_ACCOUNTING_II

P. 222

Unit 12: Standard Costing

Notes

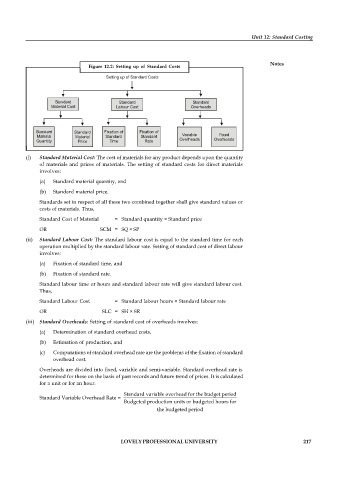

Figure 12.2: Setting up of Standard Costs

Setting up of Standard Costs

Standard Standard Standard

Material Cost Labour Cost Overheads

Standard Standard Fixation of Fixation of

Material Material Standard Standard Variable Fixed

Quantity Price Time Rate Overheads Overheads

(i) Standard Material Cost: The cost of materials for any product depends upon the quantity

of materials and prices of materials. The setting of standard costs for direct materials

involves:

(a) Standard material quantity, and

(b) Standard material price.

Standards set in respect of all these two combined together shall give standard values or

costs of materials. Thus,

Standard Cost of Material = Standard quantity × Standard price

OR SCM = SQ × SP

(ii) Standard Labour Cost: The standard labour cost is equal to the standard time for each

operation multiplied by the standard labour rate. Setting of standard cost of direct labour

involves:

(a) Fixation of standard time, and

(b) Fixation of standard rate.

Standard labour time or hours and standard labour rate will give standard labour cost.

Thus,

Standard Labour Cost = Standard labour hours × Standard labour rate

OR SLC = SH × SR

(iii) Standard Overheads: Setting of standard cost of overheads involves:

(a) Determination of standard overhead costs,

(b) Estimation of production, and

(c) Computations of standard overhead rate are the problems of the fixation of standard

overhead cost.

Overheads are divided into fixed, variable and semi-variable. Standard overhead rate is

determined for these on the basis of past records and future trend of prices. It is calculated

for a unit or for an hour.

Standard variable overhead for the budget period

Standard Variable Overhead Rate =

Budgeted production units or budgeted hours for

the budgeted period

LOVELY PROFESSIONAL UNIVERSITY 217