Page 231 - DCOM206_COST_ACCOUNTING_II

P. 231

Cost Accounting – II

Notes If the actual labour cost is lower than the standard labour cost, the variance is favourable.

On the other hand, if the actual labour cost is higher than the standard labour cost, the

variance will be adverse.

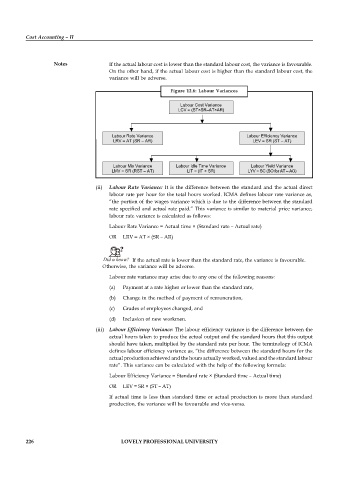

Figure 12.6: Labour Variances

Labour Cost Variance

LCV = (ST×SR–AT×AR)

Labour Rate Variance Labour Efficiency Variance

LRV = AT (SR – AR) LEV = SR (ST – AT)

Labour Mix Variance Labour Idle Time Variance Labour Yield Variance

LMV = SR (RST – AT) LIT = (IT × SR) LYV = SC (SO for AT – AO)

(ii) Labour Rate Variance: It is the difference between the standard and the actual direct

labour rate per hour for the total hours worked. ICMA defines labour rate variance as,

“the portion of the wages variance which is due to the difference between the standard

rate specified and actual rate paid.” This variance is similar to material price variance;

labour rate variance is calculated as follows:

Labour Rate Variance = Actual time × (Standard rate – Actual rate)

OR LRV = AT × (SR – AR)

Did u know? If the actual rate is lower than the standard rate, the variance is favourable.

Otherwise, the variance will be adverse.

Labour rate variance may arise due to any one of the following reasons:

(a) Payment at a rate higher or lower than the standard rate,

(b) Change in the method of payment of remuneration,

(c) Grades of employees changed, and

(d) Inclusion of new workmen.

(iii) Labour Efficiency Variance: The labour efficiency variance is the difference between the

actual hours taken to produce the actual output and the standard hours that this output

should have taken, multiplied by the standard rate per hour. The terminology of ICMA

defines labour efficiency variance as, “the difference between the standard hours for the

actual production achieved and the hours actually worked, valued and the standard labour

rate”. This variance can be calculated with the help of the following formula:

Labour Efficiency Variance = Standard rate × (Standard time – Actual time)

OR LEV = SR × (ST – AT)

If actual time is less than standard time or actual production is more than standard

production, the variance will be favourable and vice-versa.

226 LOVELY PROFESSIONAL UNIVERSITY