Page 183 - DMGT405_FINANCIAL%20MANAGEMENT

P. 183

Unit 9: Capital Budgeting

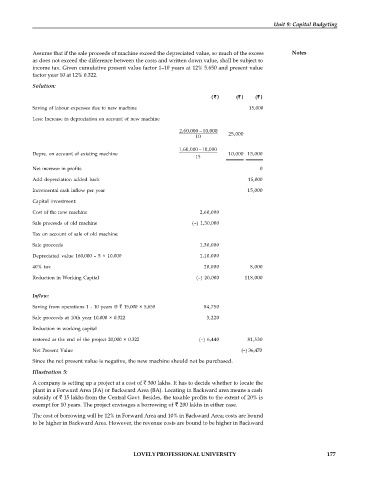

Assume that if the sale proceeds of machine exceed the depreciated value, so much of the excess Notes

as does not exceed the difference between the costs and written down value, shall be subject to

income tax. Given cumulative present value factor 1–10 years at 12% 5.650 and present value

factor year 10 at 12% 0.322.

Solution:

( (

Saving of labour expenses due to new machine 15,000

Less: Increase in depreciation on account of new machine

25,000

Depre. on account of existing machine 10,000 15,000

Net increase in profits 0

Add depreciation added back 15,000

Incremental cash inflow per year 15,000

Capital investment:

Cost of the new machine 2,60,000

Sale proceeds of old machine (–) 1,30,000

Tax on account of sale of old machine:

Sale proceeds 1,30,000

Depreciated value 160,000 – 5 × 10,000 1,10,000

40% tax 20,000 8,000

Reduction in Working Capital (–) 20,000 118,000

Inflow:

Saving from operations 1 - 10 years @ 15,000 × 5,650 84,750

Sale proceeds at 10th year 10,000 × 0.322 3,220

Reduction in working capital

restored at the end of the project 20,000 × 0.322 (–) 6,440 81,530

Net Present Value (–) 36,470

Since the net present value is negative, the new machine should not be purchased.

Illustration 5:

A company is setting up a project at a cost of 300 lakhs. It has to decide whether to locate the

plant in a Forward Area (FA) or Backward Area (BA). Locating in Backward area means a cash

subsidy of 15 lakhs from the Central Govt. Besides, the taxable profits to the extent of 20% is

exempt for 10 years. The project envisages a borrowing of 200 lakhs in either case.

The cost of borrowing will be 12% in Forward Area and 10% in Backward Area; costs are bound

to be higher in Backward Area. However, the revenue costs are bound to be higher in Backward

LOVELY PROFESSIONAL UNIVERSITY 177