Page 187 - DMGT405_FINANCIAL%20MANAGEMENT

P. 187

Unit 9: Capital Budgeting

Notes

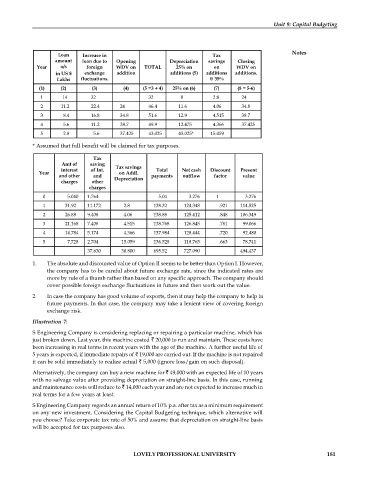

Loan Increase in Tax

amount loan due to Opening Depreciation savings Closing

Year o/s foreign WDV on TOTAL 25% on on WDV on

in US $ exchange addition additions (5) additions additions.

Lakhs fluctuations. @ 35%

(1) (2) (3) (4) (5 =3 + 4) 25% on (6) (7) (8 = 5-6)

1 14 32 32 8 2.8 24

2 11.2 22.4 24 46.4 11.6 4.06 34.8

3 8.4 16.8 34.8 51.6 12.9 4.515 38.7

4 5.6 11.2 38.7 49.9 12.475 4.366 37.425

5 2.8 5.6 37.425 43.025 43.025* 15.059

* Assumed that full benefit will be claimed for tax purposes.

Tax

Amt of saving

interest of Int. Tax savings Total Net cash Discount Present

Year on Addl.

and other and payments outflow factor value

charges other Depreciation

charges

0 5.040 1.764 5.04 3.276 1 3.276

1 31.92 11.172 2.8 138.32 124.348 .921 114.525

2 26.88 9.408 4.06 138.88 125.412 .848 106.349

3 21.168 7.408 4.515 138.768 126.845 .781 99.066

4 14.784 5.174 4.366 137.984 128.444 .720 92.480

5 7.728 2.704 15.059 136.528 118.765 .663 78.741

37.630 30.800 695.52 727.090 494.437

1. The absolute and discounted value of Option II seems to be better than Option I. However,

the company has to be careful about future exchange rate, since the indicated rates are

more by rule of a thumb rather than based on any specific approach. The company should

cover possible foreign exchange fluctuations in future and then work out the value.

2. In case the company has good volume of exports, then it may help the company to help in

future payments. In that case, the company may take a lenient view of covering foreign

exchange risk.

Illustration 7:

S Engineering Company is considering replacing or repairing a particular machine, which has

just broken down. Last year, this machine costed 20,000 to run and maintain. These costs have

been increasing in real terms in recent years with the age of the machine. A further useful life of

5 years is expected, if immediate repairs of 19,000 are carried out. If the machine is not repaired

it can be sold immediately to realize actual 5,000 (ignore loss/gain on such disposal).

Alternatively, the company can buy a new machine for 49,000 with an expected life of 10 years

with no salvage value after providing depreciation on straight-line basis. In this case, running

and maintenance costs will reduce to 14,000 each year and are not expected to increase much in

real terms for a few years at least.

S Engineering Company regards an annual return of 10% p.a. after tax as a minimum requirement

on any new investment. Considering the Capital Budgeting technique, which alternative will

you choose? Take corporate tax rate of 50% and assume that depreciation on straight-line basis

will be accepted for tax purposes also.

LOVELY PROFESSIONAL UNIVERSITY 181