Page 134 - DMGT104_FINANCIAL_ACCOUNTING

P. 134

Financial Accounting

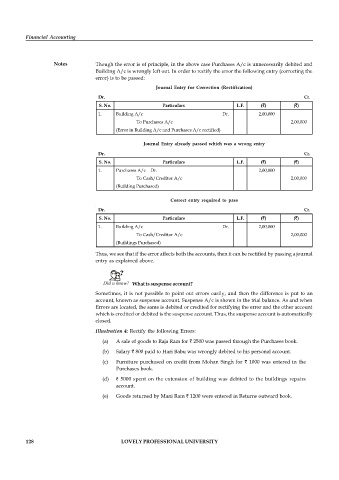

Notes Though the error is of principle, in the above case Purchases A/c is unnecessarily debited and

Building A/c is wrongly left out. In order to rectify the error the following entry (correcting the

error) is to be passed:

Journal Entry for Correction (Rectification)

Dr. Cr.

S. No. Particulars L.F. ( ) ( )

1. Building A/c Dr. 2,00,000

To Purchases A/c 2,00,000

(Error in Building A/c and Purchases A/c rectified)

Journal Entry already passed which was a wrong entry

Dr. Cr.

S. No. Particulars L.F. ( ) ( )

1. Purchases A/c Dr. 2,00,000

To Cash/Creditor A/c 2,00,000

(Building Purchased)

Correct entry required to pass

Dr. Cr.

S. No. Particulars L.F. ( ) ( )

1. Building A/c Dr. 2,00,000

To Cash/Creditor A/c 2,00,000

(Buildings Purchased)

Thus, we see that if the error affects both the accounts, then it can be rectified by passing a journal

entry as explained above.

Did u know? What is suspense account?

Sometimes, it is not possible to point out errors easily, and then the difference is put to an

account, known as suspense account. Suspense A/c is shown in the trial balance. As and when

Errors are located, the same is debited or credited for rectifying the error and the other account

which is credited or debited is the suspense account. Thus, the suspense account is automatically

closed.

Illustration 4: Rectify the following Errors:

(a) A sale of goods to Raja Ram for 2500 was passed through the Purchases book.

(b) Salary 800 paid to Hari Babu was wrongly debited to his personal account.

(c) Furniture purchased on credit from Mohan Singh for 1000 was entered in the

Purchases book.

(d) 5000 spent on the extension of building was debited to the buildings repairs

account.

(e) Goods returned by Mani Ram 1200 were entered in Returns outward book.

128 LOVELY PROFESSIONAL UNIVERSITY